Most-Favored-Nation pricing meets Joint Clinical Assessment: early evidence of compounding pressure on European drug launches

Publication: Journal of Comparative Effectiveness Research

Once it was clear to President Trump that he lacked sufficient congressional votes to get the Big Beautiful Bill approved with legislative language mandating the establishment of Most-Favored-Nations (MFN) pricing, he then signed an executive order directing the Department of Health and Human Services to pursue its powers to test and evaluate new and innovative payment systems. Subsequently, the Center for Medicare and Medicaid Innovation (CMMI) to established three pilot programs to test a US-based MFN payment policy. These three programs include GENEROUS (for all Medicaid patients), GLOBE (for 25% of Medicare Part B patients), and GUARD (for 25% of Medicare Part D patients) [1–3]. GENEROUS is a voluntary guidance program that manufacturers can choose to enroll in that mandates the use of industry reported net pricing in 19 ex-US countries, including most large European countries. In comparison, GLOBE and GUARD are mandatory proposed rules that require manufacturer participation and allow manufacturers to decide if they would prefer to utilize payment Methodology I, which is determined as the lowest per unit country-level average price reported by private research companies, or Methodology II which utilizes the weighted average net price across the same 19 designated reference countries as voluntarily reported by the manufacturer. Whereas the MFN price is updated regularly throughout the pilot under Methodology II, under Methodology I the MFN price is determined in the base year in which the product exceeds the designated annual fee-for-service spending limits and then remains fixed for the duration of the 5-year pilot program.

Selected drug products are limited to designated therapeutic categories that vary between GLOBE to GUARD, and limit inclusion to single source or sole source products. Generics, biosimilars and Inflation Reduction Act (IRA) maximum fair price-negotiated products are excluded. GLOBE targets provider-administered drugs across seven therapeutic classes (antineoplastics, immunological agents, ophthalmic agents, blood products and modifiers, CNS agents, metabolic bone disease agents and antigout agents), subject to a $100 million Part B spending threshold [3]. GUARD targets self-administered drugs across 17 therapeutic classes including analgesics, anticonvulsants, antidepressants, cardiovascular agents, immunological agents and metabolic bone disease agents, subject to a $69 million Part D threshold [3].

Given these proposed MFN rules, manufacturers are incentivized to further delay EU launches of those therapeutic classes of drugs that are scheduled to be included in GLOBE and GUARD, as well as smaller market countries included in the 19-country market basket, and countries with historically low visible reference pricing or that leak net pricing. In addition, given the new EUC Pharma Package that is scheduled to be implemented in 2028 whereby manufacturers could lose 12 months of market protections if manufacturers do not launch EMA approved medicines across all EU countries within a 3-year timeframe, we can also expect manufacturers to begin to expand the period between US FDA and EMA submissions. For the remainder of this publication, we will evaluate the impact of GLOBE and GUARD on the therapeutic category of drug launch delays seen in the EU. In future publications, we will evaluate the other factors listed above.

A recent analysis reported that pharmaceutical launches across Europe declined by 35% in the 10 months following the executive order, rising to 43% in the 14 European countries referenced by the GLOBE and GUARD models [4]. The analysis treated the European launch landscape as homogeneous; however, two features of the policy framework suggest it should not be. First, GLOBE and GUARD specify therapeutic classes, so the pattern of launch pullback might be expected to vary by class. Second, neither GLOBE nor GUARD contains an explicit orphan exclusion (in contrast to the partial orphan carve-out in the IRA), but both impose spending thresholds that should protect most rare-disease products de facto.

We have previously modelled the geographic distribution of net present value (NPV) across pharmaceutical products and shown that rest-of-world revenues account for the majority of NPV for many rare-disease therapies [5]. This implies that the calculus of delaying or withholding a European launch under MFN should depend strongly on therapeutic category, with rare-disease products having less to gain commercially from delayed European launch and more to lose.

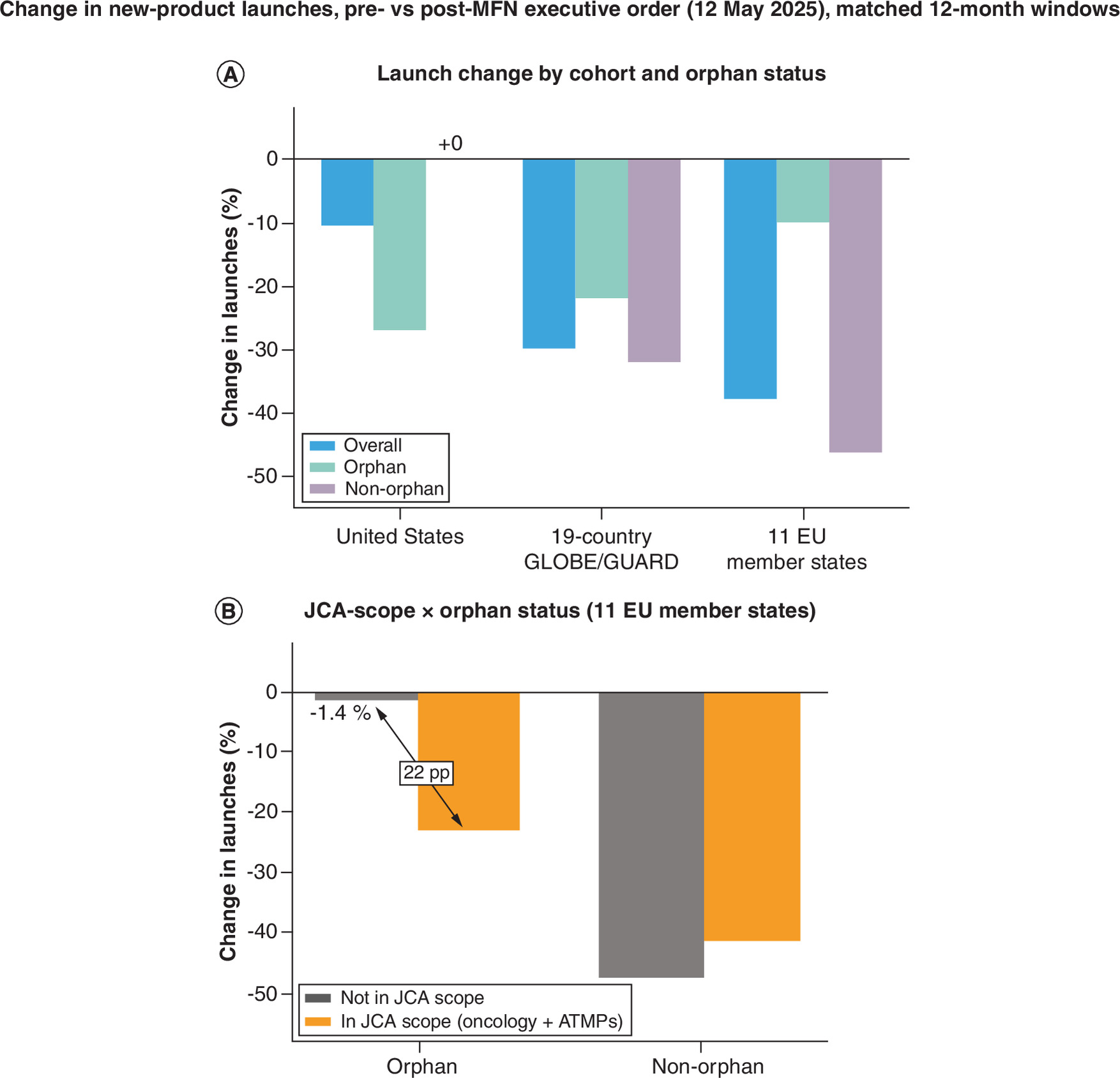

We re-examined pharmaceutical launches in Europe using an updated GlobalData extract. We compared new-product launches in matched 12-month windows (12 May 2024 to 12 May 2025 vs 12 May 2025 to 12 May 2026) across three cohorts – the 19-country GLOBE/GUARD reference basket, the 11 EU member states in this basket subject to Joint Clinical Assessment (JCA), and the US – stratifying by orphan designation, by major therapeutic area, by orphan status within therapeutic area, and by JCA scope (Figure 1 & Table 1).

Figure 1. Launch declines after the Most-Favored-Nation executive order, by orphan status and Joint Clinical Assessment scope.

Change in new-product launches before versus after the MFN executive order (12 May 2025), comparing matched 12-month windows (12 May 2024 to 12 May 2025 vs 12 May 2025 to 12 May 2026). Each launch is counted once per brand–country combination per period. (A) Launch change by cohort (USA; 19-country GLOBE/GUARD reference basket; 11 EU member states subject to JCA) and orphan status. The near-flat US non-orphan bar against steep reference-market declines is the signature of a reference-pricing spillover. (B) JCA-scope × orphan status interaction within the 11 EU member states. Among non-orphan products, JCA scope makes little difference (MFN pressure dominates regardless). Among orphan products, those outside JCA scope are essentially flat (-1.4%) while those inside JCA scope decline 22.9% – a 22-percentage-point differential, consistent with JCA preparation burden eroding the rest-of-world-NPV-driven launch resilience that orphan products otherwise show under MFN.

ATMP: Advanced therapy medicinal product; JCA: Joint Clinical Assessment; MFN: Most-Favored-Nation; NPV: Net present value.

| Subgroup | All launches | Orphan only | Non-orphan only |

|---|---|---|---|

| Total cohort (11 EU member states) | 527 → 328 (-37.8%) | 121 → 109 (-9.9%) | 406 → 219 (-46.1%) |

| By JCA scope | |||

| JCA-scope (oncology + ATMPs) | 135 → 88 (-34.8%) | 48 → 37 (-22.9%) | 87 → 51 (-41.4%) |

| Non-JCA-scope (all other classes) | 392 → 240 (-38.8%) | 73 → 72 (-1.4%) | 319 → 168 (-47.3%) |

Each launch is counted once per brand–country combination per period.

ATMP: Advanced therapy medicinal product; JCA: Joint Clinical Assessment.

Two findings emerged. First, new-product launches declined across all reference cohorts, but the magnitude tracked exposure to the policy (Figure 1A). In the 19-country GLOBE/GUARD basket, launches fell 29.9%; in the 11 EU member states subject to JCA, where MFN reference pricing and JCA preparation act together, they fell 37.8%; whereas in the US launches fell 10.5%. Orphan designation differentiated the pattern in the opposite direction in the US compared with the reference markets. In the reference cohorts, orphan-designated launches were more resilient than non-orphan launches (19-country: orphan 21.9% decline vs non-orphan 31.9% decline; 11 EU: orphan 9.9% decline vs non-orphan 46.1% decline). In the US the reverse was true: non-orphan launches were entirely flat (50 to 50; 0.0%) while orphan launches declined 26.9%. The near-flat US non-orphan figure against a 32 to 46% fall in the same products across the reference basket is the signature predicted by a reference-pricing spillover: manufacturers maintained launches in the US while pulling back from the markets whose prices anchor US MFN benchmarks. This contrast cannot be explained by a general post-2025 industry slowdown, which would have depressed US and reference-market launches alike.

Second, within the 11 EU member states – the jurisdiction in which JCA actually applies – the interaction between JCA scope and orphan status was striking. JCA-scope launches (oncology plus advanced therapy medicinal products [ATMPs], which entered mandatory JCA from 12 January 2025 [6]) showed a clear orphan-by-JCA interaction (Figure 1B). Among non-orphan products, JCA scope made little difference (in-scope 41.4% decline vs out-of-scope 47.3% decline) – the dominant MFN pressure on these US-revenue-dominated products outweighed any marginal JCA effect. Among orphan products the pattern was very different: orphan launches outside JCA scope were essentially flat (73 to 72; 1.4% decline), whereas orphan launches inside JCA scope (orphan oncology and orphan ATMPs) declined 22.9%. In other words, the only subgroup that escaped a material decline was the one exposed to neither strong MFN pressure (because rest-of-world revenues dominate its NPV) nor JCA preparation burden. The broader population and comparator scope of JCA has been flagged as a launch-delay risk independent of US pricing policy [7], and the stratified analysis here suggests these effects are already operative in orphan products currently within JCA scope.

For products in which rest-of-world revenues account for the majority of NPV – disproportionately those addressing rare conditions – the marginal damage to achievable US pricing from a European launch is small relative to the marginal damage to overall NPV from foregoing that launch. Orphan patient populations are small, the prices commanded in mature European HTA markets are typically premium, and many regulatory pathways for orphan products are tied to fixed timelines that leave limited room for strategic delay. For non-orphan products, where US revenues typically dominate NPV, the calculus is reversed: a lower European launch price now translates more directly into a lower US price, and delay or restriction of launch sequence becomes commercially defensible.

Looking forward, the JCA framework may amplify rather than mitigate MFN-related access pressure. The decline already observed in orphan products that are currently within JCA scope provides an empirical preview of what may follow the scheduled 2028 expansion of JCA to all orphan medicinal products: the resilience of orphan launches that lie outside JCA scope today may not persist once that exemption is removed, particularly as the mandatory MFN models reach operational maturity over the same period.

Several caveats apply. We are only assessing the first 12-month period after the MFN Executive Order. Additional confounders, including the ongoing revision of the EU pharmaceutical legislation, contemporaneous IRA negotiations in the US, and national cost-containment measures in several European markets, cannot be excluded. Nevertheless, the differential signal by orphan status, the orphan-by-JCA interaction, and the divergence between the US and the reference markets are large and align with predictions implicit in our prior NPV analysis.

The broader implication is that MFN-related spillover into European access has already begun and is unlikely to be uniform across drug types. The most pronounced declines so far are concentrated in non-orphan products. Orphan products have shown more launch resilience, though this resilience may not persist as JCA expands to orphan medicines in 2028. Sustaining global pharmaceutical revenues under MFN and JCA will require manufacturers to plan launches around the joint pressures both policies exert, with early and substantive investment in JCA-ready evidence becoming a prerequisite for protecting asset value.

Financial disclosure

The author received no financial and/or material support for this research or the creation of this work.

Competing interests disclosure

The authors have no competing interests or relevant affiliations with any organization or entity with the subject matter or materials discussed in the manuscript. This includes employment, consultancies, honoraria, stock ownership or options, expert testimony, grants or patents received or pending, or royalties.

Writing disclosure

No funded writing assistance was utilized in the production of this manuscript.

Open access

This work is licensed under the Attribution-NonCommercial-NoDerivatives 4.0 Unported License. To view a copy of this license, visit https://creativecommons.org/licenses/by-nc-nd/4.0/

References

1.

Delivering Most-Favored-Nation Prescription Drug Pricing to American Patients. The White House. (2025). https://www.whitehouse.gov/presidential-actions/2025/05/delivering-most-favored-nation-prescription-drug-pricing-to-american-patients/

2.

Ramagopalan SV, Pannelay AJ. Access in all areas? A round up of developments in market access and health technology assessment: part 9. J. Comp. Eff. Res. 14(10), e250120 (2025).

3.

Ramagopalan SV, Pannelay AJ. Access in all areas? A round-up of developments in market access and health technology assessment: part 13. J. Comp. Eff. Res. 15(4), e260041 (2026).

4.

Gurung S. The Most Favored Nation Policy: early insights into Europe's response. Pharma. Technol. (2026). https://www.pharmaceutical-technology.com/analyst-comment/most-favored-nation-policy-early-insights-into-europe-response/

5.

Ramagopalan SV, Thaker H, Walker M, Narasimhan O. How much do ex-US revenues make a difference for pharmaceutical investment returns? J. Comp. Eff. Res. 14(10), e250121 (2025).

6.

Ramagopalan SV, Pannelay AJ. Access in all areas? A round-up of developments in market access and health technology assessment: part 14. J. Comp. Eff. Res. 15(5), e260056 (2026).

7.

Gilardino R, Treharne C, Mardiguian S, Ramagopalan SV. Access in all areas? A round up of developments in market access and health technology assessment: part 1. J. Comp. Eff. Res. 12(10), e230129 (2023).

Information & Authors

Information

Published In

Copyright

© 2026 The author. This work is licensed under the Attribution-NonCommercial-NoDerivatives 4.0 Unported License

History

Received: 15 May 2026

Accepted: 29 May 2026

Published online: 19 June 2026

Keywords:

Topics

Authors

Metrics & Citations

Metrics

Article Usage

Article usage data only available from February 2023. Historical article usage data, showing the number of article downloads, is available upon request.

Citations

How to Cite

Most-Favored-Nation pricing meets Joint Clinical Assessment: early evidence of compounding pressure on European drug launches. (2026) Journal of Comparative Effectiveness Research. DOI: 10.57264/cer-2026-0110

Export citation

Select the citation format you wish to export for this article or chapter.