Policy perspectives on alternative models for pharmaceutical rebates: a report from the Institute for Clinical and Economic Review Policy Summit

Publication: Journal of Comparative Effectiveness Research

Abstract

Alternative approaches to the current rebate system are being considered by policymakers and stakeholders in the private insurance market. This paper presents an analysis of three alternative options to the current rebate model: retaining retroactive rebates but requiring 100% pass-through of rebates and fees to plan sponsors; retaining retroactive rebates but requiring that patients share in rebates at the point of sale; and eliminating retroactive rebates and replacing the current structure with upfront discounts. Each alternative approach presents a balance of potential advantages and disadvantages. Policymakers should not assume that switching to an alternative rebate model will deliver unalloyed benefits for patients and the health system.

The combination of rising drug costs at the health system level and increasing financial stress for individual patients has triggered intense concern in the USA. One target has come under particular scrutiny: rebates. Drug makers in the USA face no federal process whereby prices are evaluated in comparison to evidence of clinical benefit, but they must negotiate with a myriad of payers (including both insurers and pharmacy benefit managers [PBMs]). Discounts to the list price of drugs (rendered post sale as rebates) are negotiated in exchange for preferential formulary placement, which increases sales. Rebate agreements are often quite complex, including possible ‘stacked’ rebates paid to PBMs: combined payments related to formulary placement, variously named administrative fees, price increase protection guarantees and other programs.

Rebates are a key negotiating tool for payers and help produce lower net prices for drugs that can help reduce the overall costs of drug spending. But for many years the PBM business model has included a revenue stream gained by retaining a percent of the absolute rebate amount they return to plan sponsors. Drug makers argue that this ‘rebate economy’ forces them to increase list prices in order to offer larger rebates to PBMs to gain preferred formulary status. The effect of rebates in lowering net prices may reduce plan sponsor costs and moderate the cost of insurance premiums for all plan members. However, some plan sponsors argue that the profitability of rebates to PBMs provides an incentive for them to prioritize high-rebate drugs that might not have the lowest net cost for the plan sponsor. Higher list prices hurt many patients who need ongoing drug treatment, since increased use of co-insurance and of high-deductible plans has meant rising numbers of patients are required to pay their out-of-pocket share for drug coverage in relation to the list price, not the negotiated (and confidential) rebate price.

Rebates have therefore become an extremely contentious topic, praised by many as the best tool to provide competitive leverage for payers seeking lower net prices, but reviled by others who view rebates as the chief sin in a system that punishes sick patients with higher out-of-pocket costs and absorbs billions of dollars that could otherwise either reward innovative treatments, keep costs down, or both. Recently, both payers and drug makers have introduced new approaches that experiment with alternative approaches to rebates; and, in July 2019, the Trump administration abandoned a draft rule that would have expressly excluded from safe harbor protection under federal Anti-Kickback Statute any rebates paid by manufacturers to contracted PBMs or payers in Part D plans and Medicaid managed care organizations [1,2]. The Health and Human Services proposal would have created a new safe harbor for prescription drug discounts offered directly to patients, and for fixed-fee service arrangements between drug manufacturers and PBMs [2].

But amid both federal and private-market initiatives to address concerns about rebates, the potential benefits and possible negative consequences of realistic possible alternatives for different stakeholders have received little analysis. Similarly, there remain questions about how rebates interact with other elements of drug pricing, coverage and delivery.

This White Paper, benefiting from a review of relevant literature and interviews with numerous participants in the rebate process – from plan sponsors, to insurers, to PBMs, to drug makers – addresses these questions and lays out a framework for evaluating proposed alternatives to a rebate model that has served as the cornerstone of drug pricing and coverage negotiation for decades. Additional insights and recommendations resulted from a summit with leading experts and representatives from 29 insurers, pharmacy benefit management firms, drug manufacturers and biotechnology companies. A list of companies represented at the summit can be found in the acknowledgments section. This paper, however, does not reflect a consensus of opinion among summit participants [3].

How do rebates work?

The supply chain for pharmaceuticals in the USA is complex, involving many different stakeholders with competing interests. Sood et al. [4] calculate that 41% of prescription drug expenditure accrues to intermediaries in the pharmaceutical distribution system. Figure 1 illustrates the flow of services, products and payments (including rebates).

Figure 1. Simplified illustration of the flow of products, payments and services in the pharmaceutical supply chain.

Data taken from [19].

Rebates are negotiated between drug makers and payers (insurers or PBMs) when drugs first enter the market and are renegotiated on a regular or ad hoc basis. As mentioned earlier, rebates can be based on a mixture of payments from drug manufacturers to PBMs, but their primary function is to serve as an element of negotiating favorable placement within a drug formulary. For example, a company desiring its drug to be placed in the best tier of a formulary, in which the drug can be considered a ‘preferred’ drug for clinicians, with more limited drug management and low out-of-pocket payments required from patients, may offer a larger rebate off the announced list price.

Rebates are thus more common and usually larger in drug areas in which there is significant competition among branded drugs, especially when competition is among drugs with similar mechanisms of action and only incremental, if any, differences in clinical risks or benefits. Drug areas with substantial rebates include diabetes drugs and autoimmune agents used for conditions such as rheumatoid arthritis and psoriasis.

Although rebate levels are negotiated ‘upfront’ before the drugs are prescribed, they are not implemented as discounts on the price paid by the patient or even by the payer at the time of the original transaction. Instead, rebates are paid retroactively, and may include a sliding scale based on other factors such as market share or the aggregate amount of other fees wrapped into the overall rebate agreement. PBMs share all, or some portion of, rebates and other fees derived from these agreements, with the health insurer or the plan sponsor based on their contractual agreement.

The size of rebates on branded drugs varies between drugs administered through the medical benefit and those obtained through outpatient prescription drug coverage. Rebates also differ by drug types; a study of Medicare Part D rebates found that rebates were highest for drugs with brand competition (average 39% of gross cost), while protected class drugs (there are six protected classes: anticonvulsants, antidepressants, antineoplastics [including many oral chemotherapy drugs], antipsychotics, antiretrovirals, and immunosuppressants; Part D plans to cover ‘all or substantially all drugs’ within each of the classes), had lower average rebates: 14% [5]. A detailed description of how rebates function across different insurance types in the US market is beyond the scope of this paper [3].

The ‘rebate economy’ & the gross to net bubble in drug prices

Opinions on the magnitude of the difference between list and net prices following rebates, and the role that rebates play in driving overall drug expenditures, are highly contentious, differing across stakeholders and commentators. Manufacturers say that they can offer larger rebates if they increase their list prices, a view supported by some analyses linking increased overall spending on rebates with increasing list price trends [6]. Some drug companies have released aggregate net price results suggesting that net costs to the payer have declined when rebates are factored in. However, studies commissioned by the Pharmaceutical Care Management Association and the America’s Health Insurance Plans demonstrate no aggregate positive relationship between list price levels and the amount obtained in rebates [6,7].

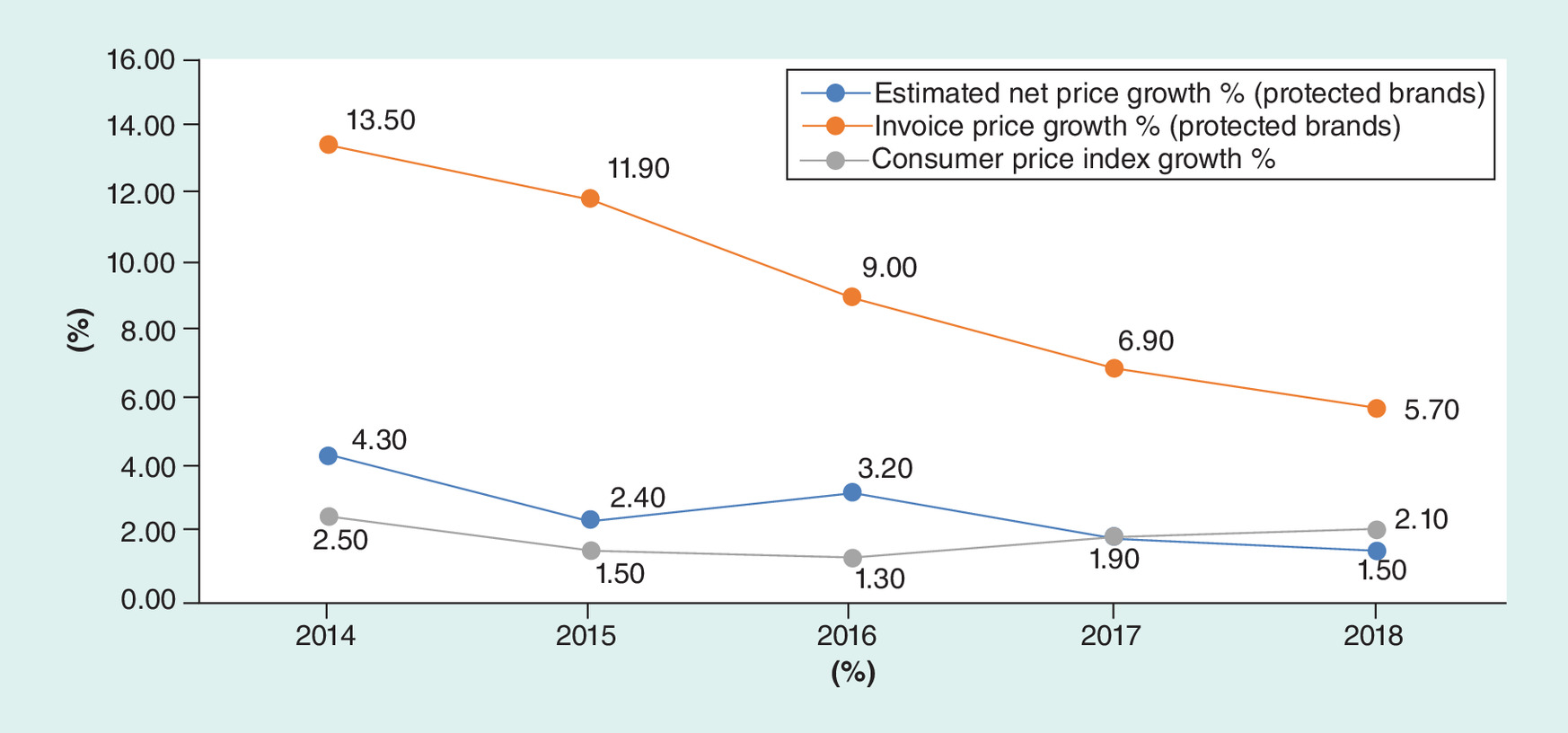

There is general agreement that the gap between list and net price is widening as a cumulative sum: over the 5 years between 2012 and 2016, the total value of pharmaceutical manufacturers’ off-invoice rebates and other price concessions more than doubled from $59 billion to $127 billion [8,9]. IQVIA Institute, a data science company the researches and forecasts global use of medicines, has shown that invoice price growth (i.e., gross price) has continually out-paced net price growth (which accounts for rebates). Both are, however, declining, with net price growth coming closer in line with general inflation. This is shown in Figure 2.

Figure 2. IQVIA: US Price Growth Comparing Brands Invoice Price and Net Price Growth 2014–2018.

Protected brands are products that have been on the market for 2 years or more and have yet to reach patent expiry.

Data taken from [18].

Data from both the Office of the Inspector General and CVS Health, a pharmacy benefit manager, corroborate this growing gap between list and net price [10,11]. In a 2018 report, the Office of the Inspector General demonstrates that while Medicare Part D reimbursement increased 62% from 2011 to 2015 ($49–80 billion), rebates more than doubled ($9–23 billion) over the same time frame [10]. CVS data also demonstrate that while gross expenditure on brand name drugs has increased, the corresponding rebate levels have increased faster, leading to the proportion of gross expenditures being rebated rising from 13% in 2011 to 31% in 2017.

For patients, the gap between list and net price can substantially affect out-of-pocket spending at the pharmacy counter. In the past decade, employers and individuals have shifted toward benefit designs with high out-of-pocket cost structures, including deductibles, co-insurance and tiered formulary design. Patients’ out-of-pocket expenditure, however, is linked to list prices instead of net prices, since net prices are considered proprietary and only determined retroactively. A large gap between list and net price therefore matters to patients, who, in some cases, might pay more out-of-pocket for the drug than its actual true (net) cost to the plan [12]. And rebate payments are made to payers even when patients are in the deductible phase of their insurance benefit and paying the full price of treatment. Examples of patients paying high out-of-pocket costs, without benefiting from the rebates negotiated for a therapy, have become commonplace in mainstream news throughout the past several years, including high profile stories about insulin and the EpiPen [13,14].

What are the major alternative options for rebate models?

There are three major alternative options to the current rebate model. The first two options represent rebate ‘reform’ and may be implemented separately or, as many have argued, combined. It is, however, important for policy makers to consider the potential advantages and disadvantages of each element separately. The third option would involve eliminating rebates and moving exclusively to a system of upfront discounts.

We evaluate each option against the following criteria:

•

Impact on patients’ affordability, access to care and clinical outcomes.

•

Impact on overall cost of pharmaceuticals and medical spending.

•

Impact on competitive outlook for innovative new medicines.

•

Ability to support outcomes-based contracting and indication-specific pricing agreements.

•

Impact on efforts to design formularies based on cost–effectiveness of pharmaceuticals.

•

Feasibility of implementation.

•

Ability to improve transparency of costs to support public dialog on value and affordability.

A summary of our evaluation of each option against these criteria is included in Table 1.

| Criteria for evaluation | Option 1: 100% pass-through of rebates to plan sponsors | Option 2: POS rebates for patients | Option 3: eliminate rebates and move to upfront discounts |

|---|---|---|---|

| Impact on patients’ affordability, access to care and clinical outcomes (via improved adherence) | With less incentive for higher rebates, list prices and gross-net gap may decline, benefiting individual patients financially if their cost sharing is linked to list price (which could lead to better adherence and outcomes). | Individual patients will see lower costs at the pharmacy counter, which could improve adherence and therefore clinical outcomes. However, the broader enrolled population may eventually face higher premiums. | Patients will have lower cost sharing based on a discounted list price. Premiums may rise, however, if bargaining power is reduced. |

| Impact on overall cost of pharmaceuticals and medical spending | If implemented comprehensively along with manufacturer fees, would increase money returned to plan sponsors and create more incentives to use low net-cost drugs. Some risk of reducing incentive for PBMs to seek lowest net price. Paying flat fees would impact the medical loss ratio calculation, which could require reductions in some plan premiums. Would not address the high computational effort and cost associated with the rebate economy. | Transparency of rebates at POS might decrease payer negotiating leverage (but depending on design, confidentiality could be maintained). Increase in plan drug costs because money returned to patients, which could lead to premium increases. Overall health costs unlikely to change unless improved adherence drives down non-drug costs. Would not address the high computational effort and cost associated with the rebate economy. | Price concessions may not be as large if transparent across all payers. However, overall drug mix in formulary design likely to change in ways that could reduce overall cost of spending. Upfront discounts could avoid the costly operational burden of rebate calculation. However, both parties will want to estimate the impact of an upfront discount on their costs. |

| Impact on competitive outlook for innovative new medicines | No improvement. If plan sponsors receive all rebates, they would have more incentive to favor existing drugs with substantial rebates over new entrant drugs with a single indication. PBMs could offer formularies favoring cost-effective new entrants and allow payers to choose lower list prices or higher list prices with larger rebates. | No direct effect. | New entrants could have improved competitive chances against existing drugs since discounts would not be linked to market share. |

| Ability to support outcomes-based contracting and indication-specific pricing agreements | As now, outcomes-based contracting and indication-specific pricing agreements are possible but limited by implementation challenges including cost. Could increase incentives for both if change leads to a greater focus on value-for-money rather than rebates. | Outcomes-based agreements require retrospective adjustment, which may be complicated by POS rebates. Implementation of indication-specific pricing may also be harder as patient indication will need to be known at POS. | Shifting to upfront discounts risks undermining progress toward meaningful outcomes-based contracts and indication-specific pricing agreements, both of which require some kind of back-end reconciliation. |

| Impact on efforts to design formularies based on cost–effectiveness of pharmaceuticals | If 100% pass-through aligns PBM and plans sponsor incentives it could facilitate adoption of value-based formularies based on cost–effectiveness. But post hoc rebates based on utilization make determination of cost–effectiveness within a formulary difficult to assign at product launch. Requires plan sponsors to shift from focus on rebates to value-for-money. | Aligning patient cost sharing with net price can facilitate the effectiveness of value-based formularies. | Prices are known for formulary design, so provides the easiest platform to construct a value-based formulary based on cost–effectiveness. |

| Feasibility of implementation | Many PBMs are already offering pass-through options. Transition over time to mandatory model for all PBM-plan sponsor contracts not significantly disruptive. | Although some PBMs are already offering this option, implementation will involve changes in contractual arrangements and information flows. | Potential issues for reconciling the many differently negotiated discounted rates for thousands of drugs along the full supply chain. There is also legal uncertainty about the feasibility of this option. |

| Ability to improve transparency of costs to support public dialog on value and affordability | While transparency for payers could be improved if accompanied by clearer dialog and understanding of rebates, public appreciation of value and affordability unlikely to be affected. | Allowing patients taking a drug to benefit directly from the rebates applied to, it is likely to support public dialog and understanding of value, but likely implementation routes are unlikely to achieve full transparency. | Transparency would be increased, which would support public dialog on value and affordability. However, it would be possible to implement upfront confidential discounts, which would maintain payer bargaining power but not increase in transparency of net prices. |

PBM: Pharmacy benefit manager; POS: Point of sale.

Option 1: 100% Pass-through (all rebates flow to plan sponsors)

The first option is to require that PBMs pass 100% of rebates and associated manufacturer fees through to plan sponsors to eliminate the incentive for PBMs to develop formularies that drive utilization to highly rebated drugs despite higher net costs for payers. PBMs would be paid through administrative fees from plan sponsors to compensate for the services they provide.

Potential advantages

With less incentive for PBMs to develop rebate-driven formularies, a 100% pass-through model would diminish financial incentives for high list prices, benefiting individual patients financially if their cost sharing is linked to list price (which could also lead to better adherence and outcomes). Net prices could remain confidential, and rebates could continue to be linked to formulary placement and utilization at the population level. Proponents believe that passing all rebates – and any other form of manufacturer fee or payment – back to plan sponsors would allow payers to compare PBM offerings more transparently, improve their negotiating power and enable them to understand why certain decisions are being made with regards to formulary design.

The law already requires that payers who participate in Medicare Part D pass back to the government all negotiated rebates, pharmacies’ fees and other forms of price concessions. The Medicare program defines these payments as direct and indirect remuneration (DIR). But policy analysts have noted that Medicare is not receiving all DIR that it is entitled to receive [15]. Prescription drug plans (PDPs) and PBMs can classify certain items to exclude them from DIR. Furthermore, if PDPs and PBMs underestimate the amount of DIR in their initial bids, they can retain a proportion of the DIR they receive beyond the initial estimation, due to the design of Part D risk corridors [15–17].

These features encourage PDPs and PBMs to favor drugs with high DIR, which are typically drugs with high list prices. A complete pass-through of DIR to Medicare, including all fees that are ‘DIR in disguise’, could therefore have a potentially significant impact on Medicare Part D prices much in the way it would in the private market. By cutting the link between PDP and PBM profit and DIR, incentives should shift toward more efficient formulary management decisions.

Last, the implementation of a pass-through model would involve relatively little disruption to the existing agreements between manufacturers and wholesalers, some of which are passed on to pharmacies and other dispensers. It would, however, still entail the challenges of a piecemeal transition from existing contracts between PBMs and plan sponsors that are not based on a 100% pass-through.

Potential disadvantages

This alternative model might achieve little if PBMs find new ways to retain revenue obtained from manufacturers as ‘fees’ instead of ‘rebates’. It would also do little for patients in the short term if the increased rebates flowing back to plan sponsors are not reflected in lower co-pays or premiums. The potential impact on the gross-to-net gap and overall spending is unclear, because many plans now expect, and some may prefer, large, guaranteed, rebates.

The primary potential advantage of a pass-through model may also represent one of its greatest potential disadvantages for both payers and patients. If PBMs are paid a fixed fee independent of negotiated rebates, they could have less incentive to put great effort into fighting for the lowest net price unless plan sponsors help create a truly different competitive landscape in which PBMs compete on the basis of patient outcomes and lowest net health system cost instead of just lowest fees.

Further, it is important to consider whether requiring PBMs to pass all rebates to plan sponsors might limit PBMs efforts to benefit from the aggregation of purchasing power to achieve greater savings beyond what a single plan could on its own. If PBMs are prohibited from aggregating rebates across multiple Part D plans, it might lead to a reduction in negotiating leverage, and therefore, higher overall net costs for payers and plan members.

Option 2: Point-of-sale rebates for patients

Point-of-sale (POS) rebates involve passing all or a proportion of rebate savings directly to patients. This option appears to most directly address high out-of-pocket costs. Some private health plans have already begun offering benefit designs with POS rebates that seek to share the financial benefits of rebates with patients, without undermining competitive leverage by allowing direct back calculation of net prices.

Potential advantages

The most important benefit of POS rebates is that patients who require extended use of expensive medications for chronic conditions could have their financial burden lessened. While evidence is limited, POS rebates could improve adherence and consequently clinical outcomes. Finally, aligning patient cost sharing with net price can facilitate the effectiveness of value-based formularies if patient co-pays are lowest, as a consequence of the POS rebates, for the most cost-effective treatment.

Potential disadvantages

POS rebates give to individual patients some of the money that would otherwise flow back to the plan sponsor. The payer no longer has the option to apply those funds in ways that reduce overall health insurance premiums. For Medicare Part D, some fear that POS rebates would lead plans to increase premiums enough to have negative effects on the affordability of plans for financially vulnerable patients. Increased premiums would also require more federal subsidy for enrollees.

POS rebates by themselves are not a cure for the financial burdens faced by many patients who need high-cost medicines. Many patients who need expensive, chronic treatment may still reach their annual out-of-pocket maximum. Furthermore, while applying POS rebates will reduce out-of-pocket cost for specific patients, they will not impact the most economically vulnerable patients on Medicaid, whose co-payments are kept low already. For these patients, as well as others who have reached the out-of-pocket maximum in their respective plans, rebate savings will continue to flow directly to the payer.

The impact of POS rebates on overall spending is unclear. Some commentators worry that POS rebates would include information for patients that inadvertently discloses the rebate level and undermines the leverage held by payers through confidential negotiations. POS rebates would also not neutralize the incentives for PBMs and others in the drug-delivery chain that may lead them to seek higher list prices and larger rebates. Another potential risk is that unless POS rebates are carefully calibrated, they could reduce the out-of-pocket cost of a branded drug to the extent that these are chosen by members in place of generics that cost less to the plan.

Option 3: Eliminate rebates & move to upfront discounts

Some commentators believe that moving to upfront discounts is both feasible and the best way to accomplish the chief aims of many stakeholders. In its draft rule, the Trump Administration took a strong stand in favor of this approach [2].

Potential advantages

The main argument for upfront discounts is that they remove the PBM incentive to generate revenue from rebates that many believe leads to higher list prices and a less transparent flow of money between manufacturers, PBMs and payers. Upfront discounts could also be the alternative model that most facilitates the application of cost–effectiveness findings to the development of formularies if prices are known and can be compared at the outset. Discounts could be allowed to vary depending on clear and uniform criteria such as formulary placement, cost–effectiveness or expected volume. If discounts were transparent, clinicians could more readily become involved in choosing the most cost-effective treatment for their patients.

Potential disadvantages

Many have argued that upfront discounts would impact payer leverage, and drug pricing behavior by drug manufacturers. For one, payers may not have the same level of leverage in negotiating upfront uniform discounts as they do in negotiating rebates that are linked to utilization/market share. The implicit transparency in upfront discounts is also viewed as problematic, potentially leading manufacturers to set single discount levels across all payers that would increase overall costs. Some have argued that publishing discounts would increase the risk of tacit collusion on price discounting among competing manufacturers. It could, however, be possible to implement upfront discounts that are confidential, so preserving bargaining power, but this puts at risk some of the benefits of increasing transparency.

Another consequence of shifting to upfront discounts is the risk of undermining progress toward meaningful outcomes-based contracts and indication-specific pricing arrangements, both of which require some kind of back-end reconciliation process. Moreover, it should not be forgotten that a legal settlement 22 years ago led to the abandonment of discounts in favor of rebates. Drug manufacturers agreed they would offer similar pricing contracts to all purchasers that demonstrated they could move market share. The legal context has not changed, so it is not clear whether manufacturers could legally offer upfront any differentiation of discounts without violating antitrust law.

From a practical perspective, a move to a fixed-price discount approach is viewed by all stakeholders as requiring a major, complicated restructuring of both Medicare Part D and commercial contracts. Wholesalers and pharmacies could end up dealing with dozens of different (discounted) prices for each drug (varying by plan) and it is not clear how such a system would move such differently priced drugs through the supply chain. It also may have significant implications for ‘best price’ rule payments by manufacturers to State Medicaid plans. Medicaid programs currently achieve large rebates and are dependent upon them to meet budgets.

Discussion

There is no perfect solution that eliminates all challenges created by rebates. Choosing the best policy option will rest on which goals are given the most weight. Stakeholders will differ as to what they most wish to see accomplished. It is possible that all three options could increase overall net costs. None directly addresses the impact of high deductible benefit designs or formularies that apply high co-insurance rates to expensive medications for chronic conditions. None would be able to solve the problem faced by manufacturers of new medicines with limited indications (and therefore market size) who are constrained in the absolute level of rebates they can offer, and therefore can be disadvantaged in formulary placement. None address drug maker launch prices or post launch drug price inflation. Many of the most expensive pharmaceuticals lack competition and thus do not come to market with any rebates. And some of the more promising efforts to use outcomes-based contracting to share risk and gain some measure of control over the effective drug price would be undercut by a move to upfront discounts. Forcing an abrupt transition away from rebates would raise significant questions about the impact on total costs of care and on patient access and outcomes. Any effort at rebate reform should also consider the broad effects of any change on potential investment decisions by drug makers.

It is conceptually attractive to consider a fourth, hybrid option, combining a POS rebate for patients with a model that also passes 100% of rebates through to plan sponsors. This combination would function in many ways like a system of upfront discounts, and could help achieve many of the same goals. There are three main differences. First, a combination of 100% pass-through and POS would not by itself re-orient the rest of the drug delivery system, that is, wholesalers and pharmacies, away from rebate incentives that favor higher list prices. Transitioning to flat fees for wholesalers and pharmacies could only be accomplished as a separate step, requiring manufacturers to take the initiative to re-contract with all elements of the delivery chain. It is unclear if market forces would compel that effort.

The second distinguishing factor between upfront discounts and a combination of 100% pass-through and POS rebate system is one that favors the latter: it would still accommodate retrospective payments needed to support outcomes-based contracts, utilization-linked rebates or the reconciliation needed for indication-specific pricing agreements. The ability to accommodate these initiatives would be viewed as a benefit by many stakeholders, and the inability of upfront discounts to readily support them is considered an important limitation.

However, the third distinguishing element between the two approaches heavily favors upfront discounts. Transparency around pricing and revenue flows is a central short-term goal held by many plan sponsors. Transparency also figures among the higher aspirations of all stakeholders who view it as a necessary driver of desired changes to the entire chain of drug pricing and delivery. Upfront discounts with transparency are more likely to support a rapid transition to flat fees for wholesalers and pharmacies along the delivery chain. Although full price transparency is viewed with alarm by some stakeholders who fear it will undermine the negotiating power of payers, it does represent the best way of assuring plan sponsors that the entire system of formulary development is not being perversely determined by the influence of rebates and hidden fees. Indeed, it maybe that some would be willing to accept higher net prices as a price worth paying, at least in the short run, for greater transparency. We also note, however, that upfront discounts could be confidential. There is a general assumption that the upfront discount model will have transparent net prices, but this may not be the case. If discounts were confidential, then bargaining power would be maintained but the benefits of transparency would be lost.

Most stakeholders in the healthcare system realize that some form of change to the current paradigm of rebates is both needed and inevitable. While there are still many unknowns regarding the ultimate financial consequences, an aspirational target of moving fully toward a system in which upfront discounts are part of a broader transformation in drug negotiation and delivery is shared by a surprising number of stakeholders. Any way forward is fraught with risk and uncertainty, with trade-offs between short-term feasibility and long-term goals evident at every step. We hope this White Paper will hearten and inform those who wish to take a thoughtful, careful approach to near-term reform while laying the groundwork for greater transformation to come.

•

Rebates are a key negotiating tool for payers to achieve competitive prices for drugs, but some stakeholders argue that they create perverse incentives that drive up list prices, and create barriers to market entry for new, innovative treatments.

•

For patients, should rebates drive high list prices, this can lead to higher out-of-pocket costs because their out-of-pocket share for drug coverage is in relation to the list price, not the negotiated rebate price.

•

This paper evaluates three major alternative options to the current rebate model to understand their impact on net drug prices, patient access and affordability, and competitive outlook for new treatments, among other criteria.

Option 1: 100% pass-through (all rebates & fees flow to plan sponsors)

•

Proponents believe that passing all rebates – and any other form of manufacturer fee or payment – back to plan sponsors would allow payers to compare pharmacy benefit manager (PBM) offerings more transparently, improve the negotiating power of payers and enable them to understand why certain decisions are being made with regards to formulary design.

•

If PBMs are paid a fixed fee independent of negotiated rebates, they could have less incentive to put great effort into fighting for the lowest net price.

OPTION 2: point-of-sale rebates for patients

•

The most important benefit of point-of-sale (POS) rebates is that patients who require extended use of expensive medications for chronic conditions could have their financial burden lessened.

•

Because POS rebates give to individual patients some of the money that would otherwise flow back to the plan sponsor; the plan sponsor can no longer apply those funds in ways that reduce overall health insurance premiums; and premiums for all members could rise.

OPTION 3: eliminate rebates & move to upfront discounts

•

The main argument for upfront discounts is that they remove the PBM incentive to generate revenue from rebates that many believe leads to higher list prices and a less transparent flow of money between manufacturers, PBMs and payers.

•

Many have argued that payers may not have the same legal and practical leverage when negotiating uniform discounts as they do in negotiating rebates that are linked to utilization/market share.

Discussion

•

It is possible that all options could increase overall net costs, and none address drug maker launch prices or postlaunch price inflation.

•

Despite the tradeoffs in rebate reform, it is conceptually attractive to consider combining a POS rebate for patients with a model that also passes 100% of rebates through to plan sponsors.

•

However, if transparency around pricing and revenue flows is a central short-term goal held by stakeholders, upfront discounts may represent the best way of assuring plan sponsors that the entire system of formulary development is not being perversely determined by the influence of rebates and hidden fees.

Disclaimer

In development of this White Paper, ICER hosted senior leaders from membership companies for an in-person meeting to deliberate on key policy recommendations for alternative models to pharmaceutical rebates. No assertion, judgment or recommendation included in the White Paper should be viewed as representing the opinion of any participant or their company. ICER alone is ultimately responsible for the final content.

Please find a list of 2018–2019 members: Aetna, Allergan, Alnylam, America’s Health Insurance Plans, Anthem, AstraZeneca, Biogen, Blue Shield of CA, Cambia Health Solutions and MedSavvy, CVS Caremark, Editas, Express Scripts, Genentech, GlaxoSmithKline, Harvard Pilgrim Health Care, Health Care Service Corporation, HealthPartners, Johnson & Johnson, Kaiser Permanente, LEO Pharma, Mallinckrodt Pharmaceuticals, Merck & Co., National Pharmaceutical Council, Novartis, Premera Blue Cross, Prime Therapeutics, Regeneron, Sanofi and United HealthCare.

Financial & competing interests disclosure

ICER receives support from pharmaceutical and health insurance companies for its membership program, including the annual ICER Policy Summit. Current members include: Aetna, Allergan, Alnylam Pharmaceuticals, America’s Health Insurance Plans, Anthem, AstraZeneca, Biogen, Blue Shield of California, Cambia Health Solutions, CVS Caremark, Editas, Express Scripts, Genentech, GlaxoSmithKline, Harvard Pilgrim Health Care, Health Care Service Corporation, HealthPartners, Johnson & Johnson, Kaiser Permanente, LEO Pharma, Mallinckrodt Pharmaceuticals, Merck & Co., National Pharmaceutical Council, Novartis, Premera Blue Cross, Prime Therapeutics, Regeneron, Sanofi and United HealthCare. ICER also receives funding from government grants and nonprofit foundations, including the Laura and John Arnold Foundation, the Commonwealth Fund, the National Institute for Health Care Management, and the New England States Consortium Systems Organization. The Office of Health Economics received a research grant from ICER to support its work in relation to the Policy Summit. The Office of Health Economics receives funding from pharmaceutical companies and from other sources for its research programs, and also operates a consulting arm, OHE Consulting. C Henshall received a fee from ICER for the time he spent contributing to the 2018 ICER Policy Summit, the background paper for it and this article. C Henshall receives fees for consultancy services relating to health technology assessment and health outcomes research and policy from various for-profit and other not-for-profit organizations working in the life sciences and health system sectors, including in 2018 the Office of Health Economics, Craig Rivers Associates International (London), The Economist Intelligence Unit (London), Ideas and Solutions (Budapest) Abbott, Medtronic and Roche. The authors have no other relevant affiliations or financial involvement with any organization or entity with a financial interest in or financial conflict with the subject matter or materials discussed in the manuscript apart from those disclosed.

No writing assistance was utilized in the production of this manuscript.

References

1.

Office of the Federal Register. Fraud and abuse; removal of safe harbor protection for rebates involving prescription pharmaceuticals and creation of new safe harbor protection for certain point-of-sale reductions in price on prescription pharmaceuticals and certain pharmacy benefit manager service fees. Washington, DC, USA (2019). https://www.federalregister.gov/documents/2019/02/06/2019-01026/fraud-and-abuse-removal-of-safe-harbor-protection-for-rebates-involving-prescription-pharmaceuticals

2.

Sachs R. Trump administrationreleases long-awaited drug rebate proposal. Health Affairs Blog (2019). https://www.healthaffairs.org/do/10.1377/hblog20190201.545950/full/?utm_source=Newsletter&utm_medium=email&utm_content=Administration+Releases+Drug+Rebate+Proposal%3B+Governors+Set+Health+Care+Agenda%3B+Caregiving%3B+The+Individual+Mandate+Penalty+In+California&utm_campaign=HAT&

3.

Cole A, Towse A, Segel C, Henshall C, Pearson S. Value, access, and incentives for innovations: policy perspectives on alternative models for rebates (2019). https://icer-review.org/material/white-paper-rebates/

4.

Sood N, Shih T, Van Nuys K, Goldman D. The Flow of Money through the Pharmaceutical Distribution System. USC Schaeffer Leonard D Schaeffer Center for Health Policy & Economics CA, USA (2017). https://healthpolicy.usc.edu/wp-content/uploads/2017/06/USC_Flow-of-MoneyWhitePaper_Final_Spreads.pdf

5.

Johnson NJ, Mills CM, Kridgen M. Prescription drug rebates and part D drug costs. Milliman Report prepared for America’s Health Insurance Plans, WA, USA (2018). https://www.ahip.org/wp-content/uploads/2018/07/AHIP-Part-D-Rebates-20180716.pdf

6.

Johnson NJ, Mills CM, Kridgen M. Prescription drug rebates and part D drug costs. Milliman Report prepared for America’s Health Insurance Plans, WA, USA (2018). https://www.ahip.org/wp-content/uploads/2018/07/AHIP-Part-D-Rebates-20180716.pdf

7.

Visante. Increasing prices set by drugmakers not correlated with rebates: an analysis prepared by Visante on behalf of PCMA (2017). https://www.pcmanet.org/wp-content/uploads/2017/06/Visante-Study-on-Prices-vs.-Rebates-FINAL.pdf

8.

Aitken M, Kleinrock M. Medicines Use and Spending in the US. A Review of 2016 and Outlook to 2021. IQVIA Institute, NC, USA (2017). https://www.iqvia.com/-/media/iqvia/pdfs/institute-reports/medicines-use-and-spending-in-the-us.pdf?_=1538408688129

9.

Fein AJ. New data show the gross-to-net rebate bubble growing even bigger. Drug Channels (2017). https://www.drugchannels.net/2017/06/new-data-show-gross-to-net-rebate.html

10.

Office of the Inspector General, US Department of Health and Human Services. Increases in reimbursement for brand-name drugs in part D (OEI-03-15-00080; 05/18)(2018). https://oig.hhs.gov/oei/reports/oei-03-15-00080.pdf

11.

CVS Health. Current and new approaches to making drugs more affordable (2018). https://cvshealth.com/sites/default/files/cvs-health-current-and-new-approaches-to-making-drugs-more-affordable.pdf

12.

Thompson M. Why a patient paid a $285 copay for a $40 drug. PBS NewsHour (2018). https://www.pbs.org/newshour/health/why-a-patient-paid-a-285-copay-for-a-40-drug

13.

Herper M. The insurance rip-off at the heart of the EpiPen scandal. Forbes (2018). https://www.forbes.com/sites/matthewherper/2016/08/30/the-consumer-rip-off-at-the-heart-of-the-epipen-scandal/#46c71685269d

14.

Tribble SJ. Why have insulin prices gone up so much? NBC News (2017). https://www.nbcnews.com/health/health-news/several-probes-target-insulin-drug-pricing-n815141

15.

Anderson G. Reforming direct and indirect remuneration in Medicare Part D. Health Affairs Blog (2019). https://www.healthaffairs.org/do/10.1377/hblog20190215.708286/full/

16.

MedPAC. Sharing risk in Medicare Part D (2015). http://www.medpac.gov/docs/default-source/reports/chapter-6-sharing-risk-in-medicare-part-d-june-2015-report-.pdf

17.

Levinson DR. Concerns with rebates in the Medicare Part D program. Department of Health and Human Services: Office of Inspector General (2011). https://oig.hhs.gov/oei/reports/oei-02-08-00050.pdf

18.

Aitken M. The Global Use of Medicine in 2019 and Outlook to 2023: Forecasts and Areas to Watch. IQVIA Institute, NC, USA (2019). https://www.iqvia.com/-/media/iqvia/pdfs/institute-reports/the-global-use-of-medicine-in-2019-and-outlook-to-2023.pdf?_=1551450951619

19.

Congressional Budget Office. Prescription Drug Pricing in the Private Sector. Congress of the United States, WA, DC (2007). https://www.cbo.gov/sites/default/files/110th-congress-2007-2008/reports/01-03-prescriptiondrug.pdf

Information & Authors

Information

Published In

Pages: 1045 - 1054

PubMed: 31559850

Copyright

© 2019 Future Medicine Ltd.

History

Received: 11 July 2019

Accepted: 12 August 2019

Published online: 27 September 2019

Keywords:

Topics

Authors

Metrics & Citations

Metrics

Article Usage

Article usage data only available from February 2023. Historical article usage data, showing the number of article downloads, is available upon request.

Citations

How to Cite

Policy perspectives on alternative models for pharmaceutical rebates: a report from the Institute for Clinical and Economic Review Policy Summit. (2019) Journal of Comparative Effectiveness Research. DOI: 10.2217/cer-2019-0094

Export citation

Select the citation format you wish to export for this article or chapter.