Why is the market design for innovative pharmaceuticals not well understood?

Publication: Journal of Comparative Effectiveness Research

The market design encouraging pharmaceutical innovation

A number of recent articles critical of the pharmaceutical industry have, in our view, betrayed a fundamental misunderstanding of its special ‘market design’. By this, we mean that market is profoundly shaped by legal and regulatory restrictions due to the US FDA, intellectual property laws and the Hatch-Waxman Act [1]. Regulatory-approved products with patent protection have a degree of monopoly – combining patent and regulatory exclusivity – that lasts on average about 13–17 years [2]. During this time, the manufacturer has the exclusive right to sell their compound, with marketing of copies being prohibited. However, this does not mean they are without competition within the same drug category. As a result, the market design for innovative medicines is characterized by oligopolistic competition among single-source products. The best product in its class may command a premium price and higher sales volume during this period of protection. However, by law, the effective market exclusivity period will eventually end, and either generics or biosimilars will be allowed to compete. The value of this monopoly power is limited by market competition and time. This leads to a market framework that promotes medical innovation by offering potentially large but uncertain returns for high-risk investments, while using competition to regulate prices in the later stages of the product lifecycle. The pharmaceutical industry largely relies on a ‘blockbuster model’, where the revenues generated by the highly successful products over the protected period must cover not only their own development costs but also the costs of the many failed products that never make it to market [3]. This failure rate is high and increasing: the probability of an oncology compound passing through all clinical trial phases and securing regulatory approval is less than 10% [4].

Misunderstanding pharmaceutical market design

As an alternative, some have argued to regulate pharmaceutical prices based on a fixed rate of return above research and development (R&D) costs, but this is impractical and, in our view, misguided. It not only fails to recognize riskiness of these investments and the irrelevance in this market design of the costs of any specific product, but also the difficulties in identifying relevant failed products and in measuring their costs. Furthermore, this perspective would fail to convey the true value of novel medicines for patients and society, and thus stifle innovation by sending no signals of value to investors in the highly risky field of drug development.

The misunderstanding of the pharmaceutical market is reflected in the recent article by Brinkhuis and colleagues that attempted to explore the relationship between the benefit of oncology treatments approved by the European Medicines Agency (EMA) and the revenues obtained from them by their manufacturers [5]. The authors concluded that most drugs recover R&D costs within a few years. They used the median R&D cost from a study by Prasad and Mailankody for their analysis. However, trying to calculate R&D costs for any one molecule is notoriously difficult, if not impossible [6]. The Prasad and Mailankody study suffers from selection bias (for example, it did not factor in the R&D costs of the many companies that went out of business and only focused on small companies where running costs are likely lower) [7], and also from information bias (for example, R&D costs likely occurred at companies before the time periods that they analyzed) [8]. Similar studies trying to calculate R&D costs are also afflicted by various issues (e.g., the study by Wouters et al. which was unable to truly ascribe preclinical costs to a specific drug [9]). Moreover, even in the unlikely event that all R&D expenses are accurately accounted for, this would still be irrelevant [10]. Manufacturers do not price specific medicines based on their own R&D costs: market-based drug prices ultimately reflect the value and benefits they offer to patients, caregivers, healthcare systems and society as a whole [10,11]. Pharmaceutical companies conduct pharmacoeconomic studies to demonstrate the cost–effectiveness of their new medicines. Payers assess these studies and negotiate prices and access conditions for specific products. In this market context, a new drug that more effectively addresses health problems or provides a solution to a previously unsolved issue will generally command a higher price than existing alternatives. Indeed, Brinkhuis and colleagues found that higher added benefit ratings for oncology treatments investigated (despite this being defined predominantly by HTA agencies, who often only provide a narrow assessment on the value of new therapies [1,12]) were generally accompanied by greater revenues. This also explains the ‘high’ initial prices of hepatitis C treatments, which offered significant new value over previous therapies [11,13]. The prices of these drugs were not set based on the amount spent on R&D: rather, they reflected the remarkable benefits these drugs delivered to patients and healthcare systems, reducing future costs associated with more expensive medical interventions and improving patient life expectancy and quality of life. Importantly, the race to bring these new drugs to market involved multiple competitors. As subsequent companies introduced rival hepatitis C treatments, prices decreased due to the availability of alternatives, prompting sellers to negotiate lower prices through discounts and rebates. The incentives created by market-based prices drive innovation, which in turn can lead to price reductions.

The role of HEOR professionals in communicating the pharmaceutical market design

It is crucial for health economics and outcomes research (HEOR) professionals to take a more active role in effectively communicating the intricacies of the pharmaceutical market design to policymakers, healthcare stakeholders, and the general public. Analyses such as that by Brinkhuis and colleagues make an implicit suggestion that pharmaceuticals should follow a ‘cost-plus’ marketplace with a regulated rate of return, and this receives widespread attention. Notably, Senator Bernie Sanders has recently asked Novo Nordisk for the R&D costs of semaglutide, a treatment for obesity [14]. It is imperative that we communicate that using R&D costs to determine pricing is flawed and instead focus should be made on estimating the full value that a medicine provides to patients, their families and society. The ‘blockbuster model’ (illustrated in Figure 1) [15], which relies on the revenues of successful drugs to cover the costs of the many failed attempts, is often misunderstood or overlooked in discussions about drug pricing and regulation. Of course, companies can still make profit on a ‘marginal’ product if the revenues cover the marginal R&D cost and costs of production and distribution; but a company needs a few products averaging multiples of average R&D cost to cover the failed products. This lack of understanding can lead to the implementation of misguided policies, such as price controls based on simplistic cost-plus formulas, which fail to account for the high failure rates and the true costs of bringing a new drug to market. If such policies become more widespread, they could have severe consequences for the pharmaceutical industry, leading to reduced investment in R&D, and ultimately resulting in fewer innovative treatments reaching patients.

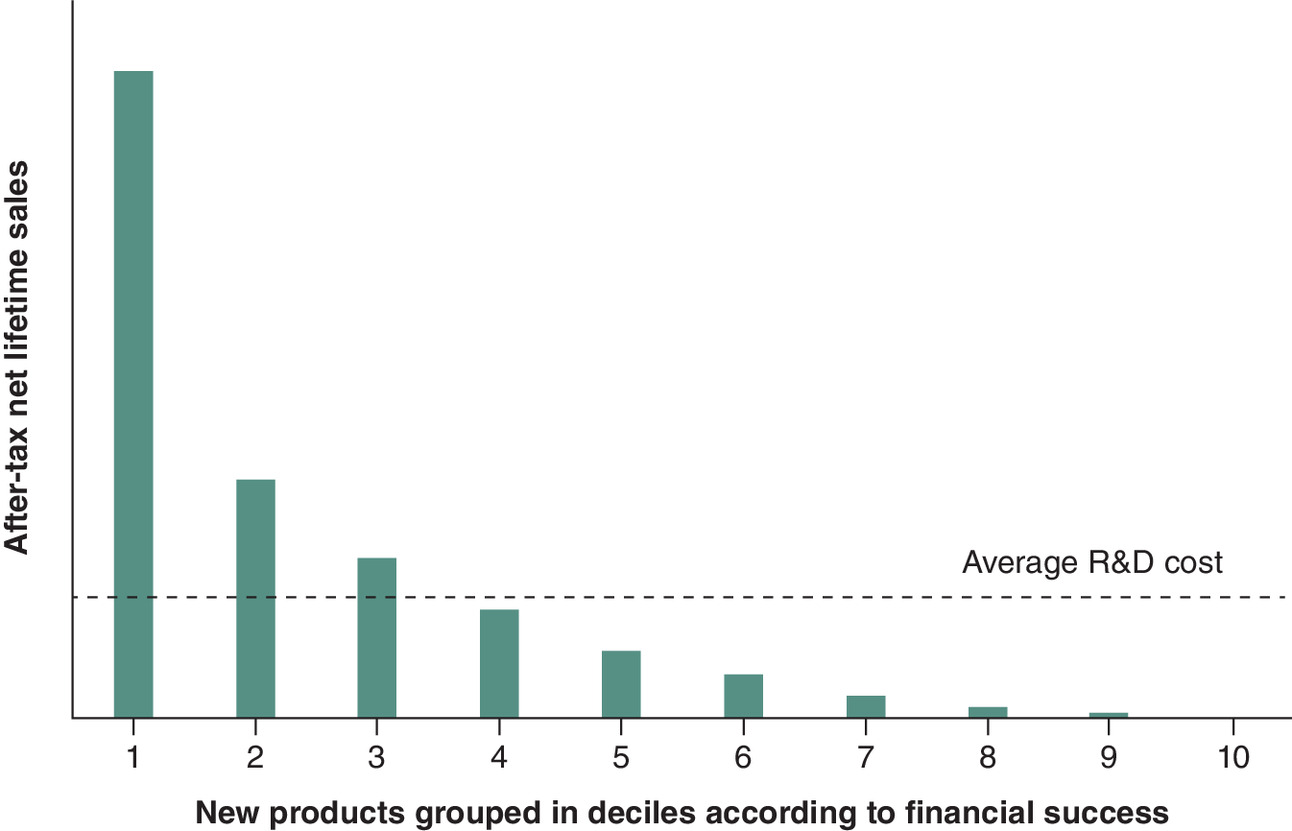

Figure 1. Illustration of the ‘blockbuster model’.

The model relies on revenues arising from the small fraction of successful drugs to support high risk, high reward investment in the entire industry which has a high rate of failure. As such, it is irrelevant to calculate the cost of developing a single drug.

Adapted from Grabowski et al. with permission from [15].

R&D: Research and development.

Financial disclosure

F Olivença and SV Ramagopalan are employees of Lane Clark & Peacock LLP. J Diaz is an employee of Bristol Myers Squibb. LP Garrison consults to life sciences organizations. The authors have no other relevant affiliations or financial involvement with any organization or entity with a financial interest in or financial conflict with the subject matter or materials discussed in the manuscript apart from those disclosed.

Competing interests disclosure

The authors have no competing interests or relevant affiliations with any organization or entity with the subject matter or materials discussed in the manuscript. This includes employment, consultancies, honoraria, stock ownership or options, expert testimony, grants or patents received or pending, or royalties.

Writing disclosure

No writing assistance was utilized in the production of this manuscript.

Acknowledgments

SV Ramagopalan acknowledges helpful discussions with Dr Charlotte McIntyre and Prof. Amil Dasgupta.

Open access

This work is licensed under the Attribution-NonCommercial-NoDerivatives 4.0 Unported License. To view a copy of this license, visit https://creativecommons.org/licenses/by-nc-nd/4.0/

References

1.

Ramagopalan SV, Diaz J, Mitchell G, Garrison LP Jr, Kolchinsky P. Is the price right? Paying for value today to get more value tomorrow. BMC Med. 22(1), 45 (2024).

2.

Rome BN, Lee CC, Kesselheim AS. Market exclusivity length for drugs with new generic or biosimilar competition, 2012–2018. Clin. Pharmacol. Ther. 109(2), 367–371 (2021).

3.

Schuhmacher A, Hinder M, Boger N, Hartl D, Gassmann O. The significance of blockbusters in the pharmaceutical industry. Nat. Rev. Drug Discov. 22(3), 177–178 (2023).

4.

IQVIA Institute for Human Data Science. Global Oncology Trends 2023: outlook to 2027 (2023). https://www.iqvia.com/-/media/iqvia/pdfs/institute-reports/global-oncology-trends-2023/iqvia-institute-global-oncology-trends-2023-forweb.pdf (Accessed 6 June 2024).

5.

Brinkhuis F, Goettsch WG, Mantel-Teeuwisse AK, Bloem LT. Added benefit and revenues of oncology drugs approved by the European Medicines Agency between 1995 and 2020: retrospective cohort study. BMJ 384, e077391 (2024).

6.

Prasad V, Mailankody S. Research and development spending to bring a single cancer drug to market and revenues after approval. JAMA Intern. Med. 177(11), 1569–1575 (2017).

7.

van der Gronde T, Pieters T. Assessing pharmaceutical research and development costs. JAMA Intern. Med. 178(4), 587–588 (2018).

8.

DiMasi JA. Assessing pharmaceutical research and development costs. JAMA Intern. Med. 178(4), 587 (2018).

9.

Wouters OJ, McKee M, Luyten J. Estimated research and development investment needed to bring a new medicine to market, 2009–2018. JAMA 323(9), 844–853 (2020).

10.

Garrison LP Jr, Towse A. The IRA's Request For Product-Specific R&D cost information: short-sighted and irrelevant. Health Affairs Forefront (2023). https://www.healthaffairs.org/content/forefront/ira-s-request-product-specific-r-d-cost-information-short-sighted-and-irrelevant (Accessed 6 June 2024).

11.

Grabowski H, Manning R. Drug prices and medical innovation: a response to Yu, Helms, and Bach. Health Affairs Forefront (2017). https://www.healthaffairs.org/content/forefront/drug-prices-and-medical-innovation-response-yu-helms-and-bach (Accessed 6 June 2024).

12.

Ramagopalan SV, Treharne C, Pearson-Stuttard J, Subbiah V. For what it's worth: the complex area of medicine value assessment. J. Comp. Eff. Res. 12(9), e230120 (2023).

13.

Garrison LP Jr, Jiao B, Elsisi Z et al. Estimating the allocation of the economic value generated by utilization of all-oral direct-acting antivirals for hepatitis C in the United States, 2015 to 2019. Value Health. 27(8), 1021–1029 (2024).

14.

Sanders B. Letter to the CEO of Novo Nordisk. (2024). https://www.sanders.senate.gov/wp-content/uploads/Letter-from-Sen.-Bernard-Sanders-to-Novo-Nordisk.pdf (Accessed 6 June 2024).

15.

Grabowski H, Vernon J, DiMasi JA. Returns on research and development for 1990s new drug introductions. Pharmacoeconomics 20(Suppl. 3), 11–29 (2002).

Information & Authors

Information

Published In

Copyright

© 2024 The authors. This work is licensed under the Attribution-NonCommercial-NoDerivatives 4.0 Unported License

History

Received: 3 July 2024

Accepted: 30 August 2024

Published online: 10 September 2024

Keywords:

Topics

Authors

Metrics & Citations

Metrics

Article Usage

Article usage data only available from February 2023. Historical article usage data, showing the number of article downloads, is available upon request.

Citations

How to Cite

Why is the market design for innovative pharmaceuticals not well understood?. (2024) Journal of Comparative Effectiveness Research. DOI: 10.57264/cer-2024-0105

Export citation

Select the citation format you wish to export for this article or chapter.

Citing Literature

- Joseph Twomey, Leonhard Kersten, Edward W. Zhou, Fred D. Ledley, Contribution of revenue from drugs subject to price negotiation under the Inflation Reduction Act to the revenue, profit, and returns of pharmaceutical manufacturers, Drug Discovery Today, 10.1016/j.drudis.2025.104585, 31, 1, (104585), (2026).

- Sreeram V Ramagopalan, Catherine Bacon, Mel Walker, Michael L Ryan, The need to consider market access for pharmaceutical investment decisions: a primer, Journal of Comparative Effectiveness Research, 10.57264/cer-2025-0036, 14, 5, (2025).