Employer-perspective cost comparison of surgical treatments for abnormal uterine bleeding

Publication: Journal of Comparative Effectiveness Research

Abstract

Aim: To estimate direct and indirect costs of surgical treatment of abnormal uterine bleeding (AUB) from a self-insured employer's perspective. Methods: Employer-sponsored insurance claims data were analyzed to estimate costs owing to absence and short-term disability 1 year following global endometrial ablation (GEA), outpatient hysterectomy (OPH) and inpatient hysterectomy (IPH). Results: Costs for women who had GEA are substantially less than costs for women who had either OPH or IPH, with the difference ranging from approximately $7700 to approximately $10,000 for direct costs and approximately $4200 to approximately $4600 for indirect costs. Women who had GEA missed 21.8–24.0 fewer works days. Conclusion: Study results suggest lower healthcare costs associated with GEA versus OPH or IPH from a self-insured employer perspective.

Lay abstract

This study shows lower costs from an employer's perspective for treating abnormal uterine bleeding with global endometrial ablation versus inpatient and outpatient hysterectomy. Total direct and indirect cost savings associated with global endometrial ablation in the year following intervention are estimated to be as much as $15,000. Healthcare providers should be aware that choice about the type of surgical treatment of abnormal uterine bleeding impacts a woman's work attendance and the cost burden to her employer.

Abnormal uterine bleeding (AUB) is a gynecologic disorder involving bleeding from the uterus that differs in frequency, regularity, duration or amount from normal uterine bleeding in the absence of pregnancy [1]. AUB affects about 10–30% of women of reproductive age, impacting >10 million women each year [2,3]. AUB can profoundly interfere with a woman's physical, social and/or material quality of life [2,4–8]. Importantly, because AUB primarily impacts women in the working-age group, the condition can have a detrimental impact on a woman's ability to perform paid work, with potential financial ramifications for both herself and her employer [2,9]. Because AUB is an expensive condition to endure and to treat, choice of treatments can profoundly affect the magnitude of those costs [8,10,11].

Typical conservative management of AUB comprises watchful waiting and pharmacological therapy [1,12]. Surgical treatments for AUB are available for pathological cases (e.g., polyps, fibroids), when symptoms become intolerable and the patient does not respond to medical therapy or becomes refractory to medical treatment, or for when surgery becomes a patient's personal choice [13]. Hysterectomy is the most common and invariable successful surgical treatment for AUB. Regardless of surgical route, laparoscopic/robotic-assisted, vaginal, or abdominal, hysterectomy is considered a major operation with a lengthy recovery period fraught with morbidity and rare instances of mortality, as well as high healthcare costs [10,11,13–15]. Alternatively, global endometrial ablation (GEA) is a minimally invasive technique for surgically destructing the endometrium (while preserving the uterus) that can be performed without general anesthesia in an outpatient setting [16–18]. The procedure has fewer adverse effects, a shorter recovery period and substantially lower costs compared with hysterectomy [10,11,16–18]. All of these positive qualities translate into financial benefits for healthcare payers seeking safe, cost-effective AUB treatments and for employers who want women to return to work as quickly as possible.

Few studies have evaluated direct costs of AUB treatments and the impact that AUB treatments have on work productivity and associated indirect costs. Most evaluations have focused on the work impact of AUB itself [2,9,19], although some studies have evaluated the impact of AUB pharmacotherapies on productivity [20,21]. Cost comparison analyses for surgical treatment of AUB from a self-insured employer perspective have not yet been undertaken. In this study, we analyzed insurance claims data to estimate direct and indirect costs of surgical treatment of AUB with GEA, outpatient hysterectomy (OPH) and inpatient hysterectomy (IPH) from a self-insured employer perspective.

Methods

Data sources

Data were extracted from a subset of the IBM® MarketScan® Commercial Database called the IBM® MarketScan® Health and Productivity Management (HPM) Database [22,23]. The MarketScan HPM Database combines data on workplace absence, short- and long-term disability and workers’ compensation with concurrent histories of medical/surgical claims and outpatient drug data claims of employees whose productivity is being measured. These linked data conveniently allow researchers to evaluate both the direct and indirect costs of illness and disease. Data in the MarketScan HPM Database are de-identified and comply with the Health Insurance Portability and Accountability Act (HIPAA) regulations. Thus, Institutional Review Board approval was not required to conduct this study.

Employers contributing to the MarketScan HPM Database routinely measure paid absenteeism, the most obvious form of productivity loss, because it involves explicit monetary costs. The MarketScan HPM Database captures episodes of paid leave (i.e., work days on which the employee was absent for part or all of the day) and short-term disability (STD; i.e., absence from work due to an approved disability claim), as documented in the payroll systems of employers who contribute data to the database. By applying exogenous wage rate and work-hours data to the MarketScan HPM work absence data, indirect cost evaluation can be conducted on these patients. In summary, the MarketScan HPM Database is a substantial data resource for conducting studies on the direct and indirect cost of illness. The database is robust and large enough to allow creation of a representative data sample of women with AUB and particularly well-suited for evaluating employer-perspective costs of AUB treatments.

AUB treatment cohorts analyzed

The MarketScan HPM Database was used to identify female employees aged 30–55 years with AUB who had GEA, OPH or IPH during 1 January 2013–30 June 2015. The GEA cohort encompassed the blend of uterine ablation modalities currently utilized in the US real-world treatment settings including bipolar radiofrequency ablation and all other second-generation GEA techniques (e.g., cryotherapy, microwave endometrial ablation, thermal balloon endometrial ablation, hydrothermal ablation). Similarly, the OPH and IPH cohorts represented composites of real-world utilization of laparoscopic/robotic-assisted hysterectomy, vaginal hysterectomy and abdominal hysterectomy.

Patients selected for the analysis were required to have ≥12 months of continuous enrollment with medical and pharmacy benefits in the database before intervention and ≥12 months of continuous enrollment with medical and pharmacy benefits after the intervention. Patients were excluded if in the 12-month preintervention period they were menopausal or had claims for GEA or hysterectomy. Patients also were excluded if they had claims for pregnancy or birth in the 12-month preintervention or 12-month postintervention period. Also, patients with primary cancer (except skin cancer) in the 12-month preintervention or 12-month postintervention period were excluded. OPH and IPH were defined by the specific setting in which hysterectomies were performed (i.e., ‘outpatient’ vs ‘inpatient’ treatment setting), as integrally flagged in the claims data. Generally, IPH requires a hospital admission whereas OPH can occur in a hospital if the patient is not formally admitted.

After applying inclusion/exclusion criteria, a total of 56,665 patients (GEA: 31,629; OPH: 14,548; IPH: 10,488) factored into the plan-paid direct cost analyses, while a total of 898 patients with absenteeism data and 7128 patients with STD data were included in the indirect cost analyses. The dataset used for the work absence and productivity cost analyses retained all the patients regardless of the number of days of paid absence they incurred, including the patients who had no days of absence, so the statistical tabulations are truly reflective of any given woman who had surgical treatment of her AUB, not just those women in the subset who have work absence. Consequently, the absence and STD analysis estimates are additive (i.e., days of paid absence plus days of STD sum to total days of absence) and are presented here both in composite and disaggregated form. Because STD often initiates only after expenditure of vacation and sick days, it is likely that most STD patients also had work absence, but coinciding data were lacking or claims coding was inconsistent in that regard. To simplify the scope of the study analyses, no attempt was made to separately analyze the small subset of patients who had claims records for both paid absence and STD.

Cost accounting

Costs included direct costs from adjudicated claims that were paid by employers for provision of healthcare to employees, and indirect costs associated with work impairment (i.e., lost work time due to absence and disability). Direct costs included costs of AUB surgical intervention, complications and reintervention (for GEA patients), along with all other healthcare costs incurred 1-year postsurgery. For exploration, the subsets of total healthcare costs that were gynecologic related were analyzed separately. Another set of analyses disaggregated total healthcare costs by ten employer-type classifications to determine how costs might vary across different industries in which patients were employed.

Indirect costs of absenteeism and STD were imputed using the so-called ‘human capital approach’, which uses wages as a conservative proxy measure of work time output [24–26]. This was accomplished by multiplying the number of hours of absence by a wage constant specific to women in the age group (i.e., $23.88/h, calculated from a median weekly wage of $824 divided by the average 34.5 h worked per week) [27,28]. Although sometimes it is a practice in health economic analyses to adjust the STD wage rate downward to reflect the typical approximately 60% fixed percent of earnings that employees receive as an STD benefit [29], our analyses assume that the cost of lost work time is oriented from a true employer's perspective, reflecting the complete impact of losing the productivity of the disabled worker, including staff substitution/replacement costs or diminished/precluded production costs that may arise from STD absences. Therefore, for both simplicity and consistency, the same wage constant of $23.88 was applied to STD absences in the analyses presented here. All costs from the analyses in this study are presented as 2017 US dollars.

Analyses & outcomes

Analyses of the data were conducted to estimate 1-year direct costs of healthcare for patients who underwent GEA, OPH and IPH, with results disaggregated by gynecologic-related costs and all other healthcare costs. Total direct costs for GEA, OPH and IPH also were disaggregated by ten industry type classifications. Similar analyses were conducted to estimate work productivity outcomes, which included total and incremental number of work days lost due to paid absence and STD. Corresponding total and incremental wage-related indirect cost estimates were calculated based on the worker absence results.

To test the potential impact of differences in the demographic and health history profiles between patients in each respective surgical treatment cohort, an exploratory multivariate analysis of the 1-year healthcare cost results was conducted using generalized linear model regressions with a log link function. The regressions were specified to control for patient age, geographic region of patient residence and whether that residence was in an urban or rural setting, comorbid conditions, baseline medication utilization and baseline healthcare costs in the year prior to surgery. Two separate models were specified – one to compare GEA versus OPH and the other to compare GEA versus IPH – with the primary end point of interest being the 1-year healthcare costs following surgical treatment of AUB.

Results

Total 1-year healthcare costs paid by employer-sponsored insurance for women with surgical AUB treatment were $14,715 for GEA, $22,425 for OPH and $24,749 for IPH, with cost savings of GEA versus hysterectomy ranging from $7709 to $10,033 in the comparisons with OPH and IPH, respectively (Figure 1). The subset of gynecology-related costs was more than a half of total costs across all treatments, although appreciably less for GEA (55%) than for OPH (66%) and IPH (65%). Gynecology-related costs also were comparatively lower for GEA treatment relative to hysterectomy, with cost differences ranging from $6648 to $8077 in the comparisons against OPH and IPH, respectively (Figure 1).

Figure 1. Comparative 1-year employer-paid direct healthcare costs.

GEA: Global endometrial ablation; IPH: Inpatient hysterectomy; OPH: Outpatient hysterectomy.

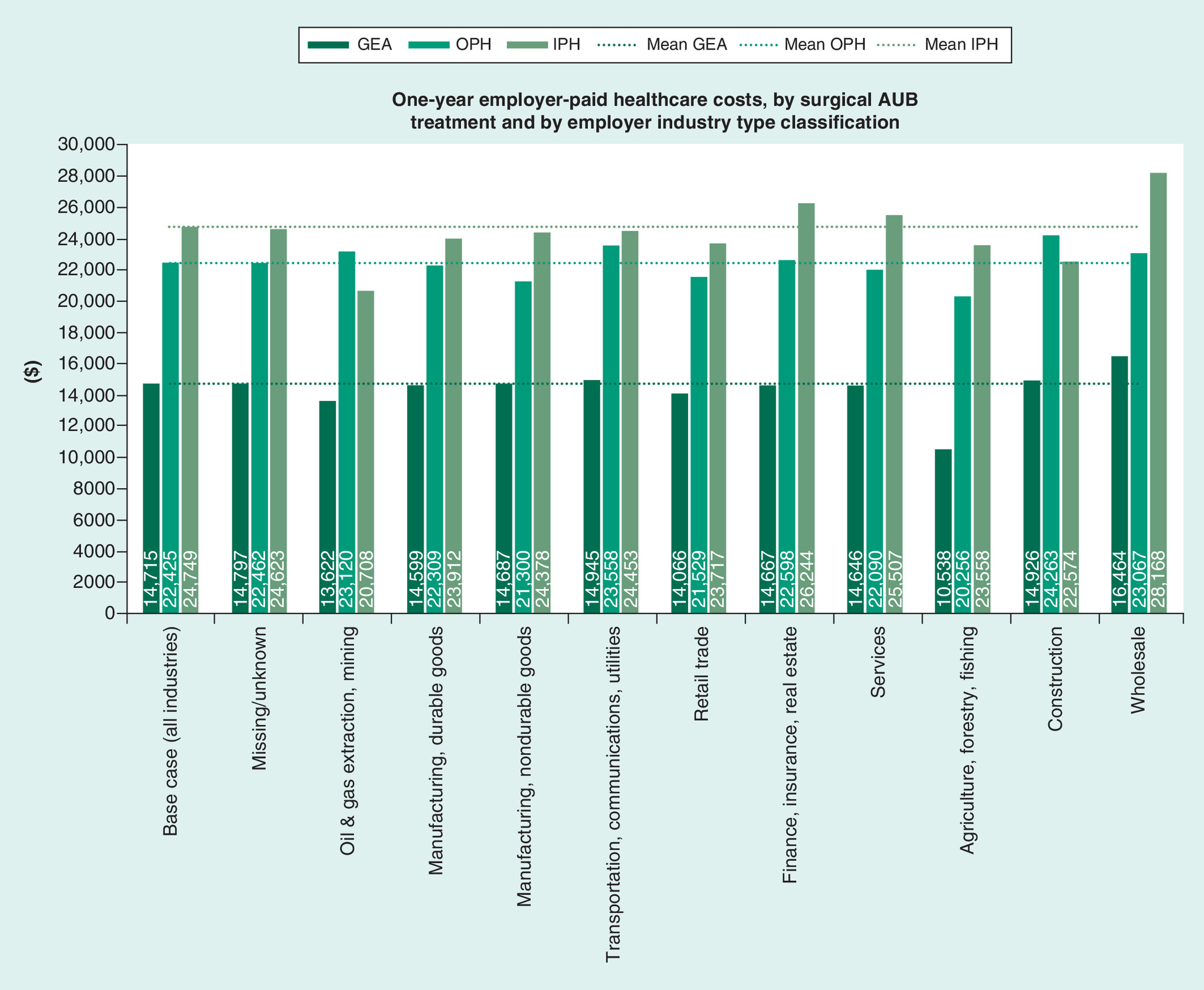

Costs varied when disaggregated by industry type. The largest deviations from the base case analysis results (i.e., the blend of all industry types) were found in GEA for ‘agriculture/forestry/fishing’ (28.4% lower costs) and in IPH for ‘wholesale’ (13.8% higher costs) (Figure 2). Cost differences for GEA versus OPH and IPH were greatest for patients employed in ‘agriculture/forestry/fishing’ ($9718 for GEA vs OPH; $13,020 for GEA vs IPH), followed by sizeable differences across other industries.

Figure 2. One-year employer-paid healthcare costs, by surgical treatment and by employer industry type classification.

AUB: Abnormal uterine bleeding; GEA: Global endometrial ablation; IPH: Inpatient hysterectomy; OPH: Outpatient hysterectomy.

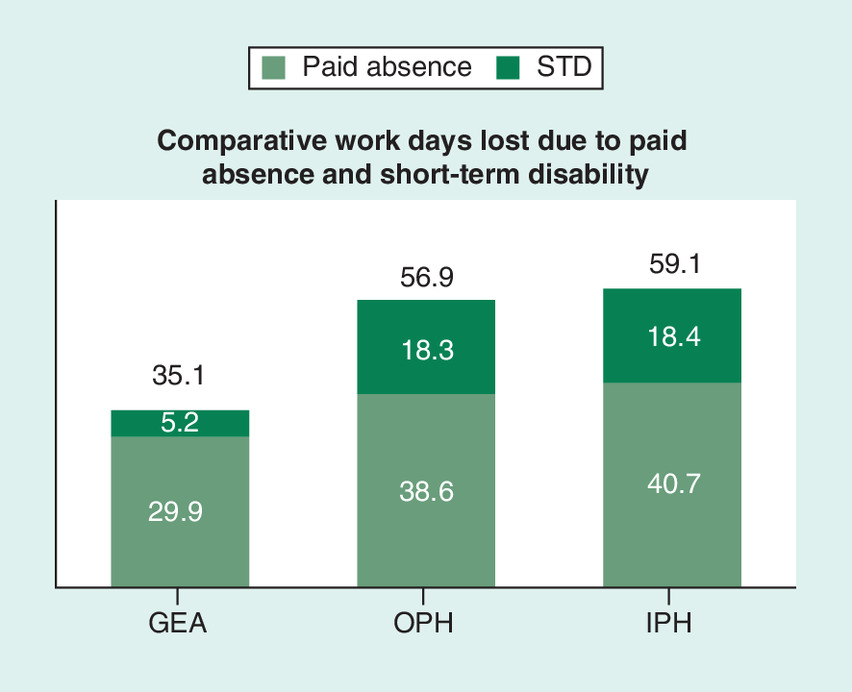

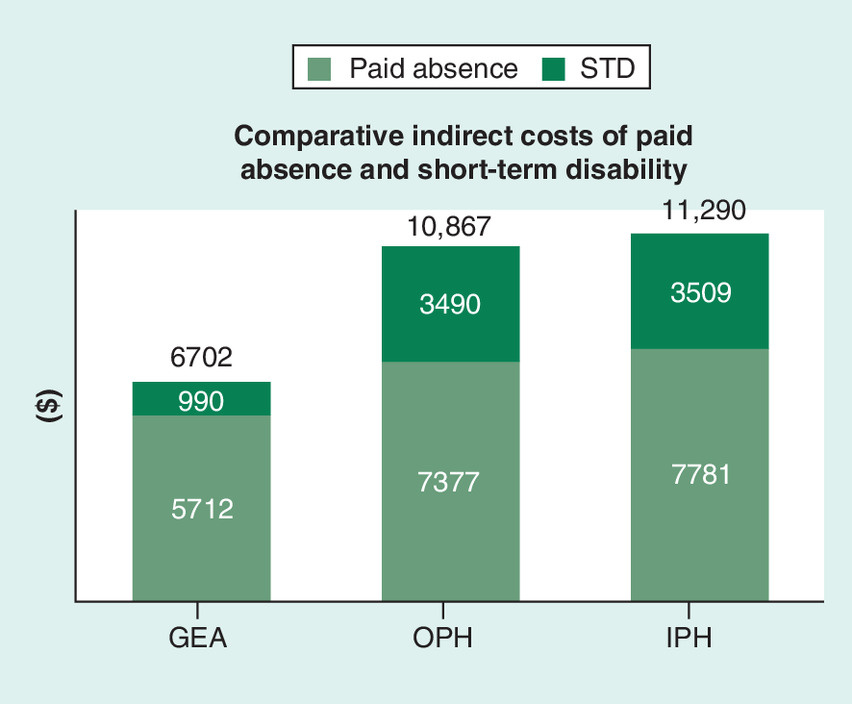

As shown in Figure 3, GEA patients were absent from work for a total of 35.1 days in the year following surgery (29.9 days due to paid absence, 5.2 days due to STD), compared with 56.9 days for OPH (38.6 days due to paid absence, 18.3 days due to STD) and 59.1 days for IPH (40.7 days due to paid absence, 18.4 days due to STD). Comparatively, paid absence was 8.7 days less for GEA versus OPH and 10.8 days less for GEA versus IPH, while STD absence was 13.1 days less for GEA versus OPH and 13.2 days less for GEA versus IPH. After applying the wage rate to these results, corresponding total indirect costs of paid absence plus STD were $6702 for GEA compared with $10,867 for OPH and $11,290 for IPH, with the net difference in indirect cost ranging from $4165 for GEA versus OPH to $4588 for GEA versus IPH (Figure 4).

Figure 3. Comparative work days lost due to paid absence and short-term disability.

GEA: Global endometrial ablation; IPH: Inpatient hysterectomy; OPH: Outpatient hysterectomy; STD: Short-term disability.

Figure 4. Comparative indirect costs of paid absence and short-term disability.

GEA: Global endometrial ablation; IPH: Inpatient hysterectomy; OPH: Outpatient hysterectomy; STD: Short-term disability.

Exploratory multivariate analysis

There were observable differences between GEA and hysterectomy patients included in the analysis with regard to their demographics and health histories. For example, hysterectomy patients were about a half year older than GEA patients and were more likely to live in rural areas of southern US states. Also, hysterectomy patients generally had higher prevalence of comorbid conditions, including endometriosis, dysmenorrhea, uterine fibroids/polyps and urinary incontinence. Overall medication utilization was similar, but hysterectomy patients were more likely to use oral contraceptives.

Given that this study was a descriptive analysis of real-world claims data (i.e., portraying the actual imposition that surgical treatments have on productivity and healthcare costs that are borne by self-insured employers), no adjustments were made in the core analysis for sociodemographic and clinical factors that may have influenced choices in surgical treatment of AUB and other healthcare utilization behaviors. However, results from the exploratory multivariate analysis were informative to evaluate the potential impact that differences in baseline characteristics of patients may have had on healthcare costs in the year following GEA, OPH and IPH.

After multivariate adjustment, 1-year postsurgical healthcare costs were still significantly (p < 0.0001) higher for both OPH and IPH compared with GEA, albeit the relative differences were approximately $1100–$2100 less than those estimated in the core, descriptive analysis reported above. In the multivariate analysis, total 1-year healthcare costs paid by employer-sponsored insurance for women with surgical AUB treatment with GEA were $15,364 (mean of the estimates from the two multivariate models), compared with $14,715 in the core analysis. Hysterectomy costs were $21,956 for OPH (versus $22,425 in the core analysis), and $23,339 for IPH (versus $24,749 in the core analysis). By way of incremental comparison, relative cost savings of GEA versus hysterectomy ranged from $6646 to $7922 matched against OPH and IPH, respectively (compared with $7709–$10,033 in the core analysis). These findings indicate that differences in attributes between the surgical treatment groups had only a modest influence on the cost results.

Discussion

Our study analyzed insurance claims data for large cohorts of women who had surgical treatment of their AUB in order to estimate their employer-sponsored healthcare costs and impact on work productivity in the year after their surgery. To our knowledge, this is the first study to specifically evaluate comparative costs of GEA and hysterectomy from an employer's perspective. We found that postsurgical healthcare costs for women with AUB are substantial, ranging from about $15,000 to $25,000 in direct costs and another $7000 to $11,000 in indirect costs, depending on choice of surgery. As would be expected, costs for women who had hysterectomy in the outpatient setting (OPH) were less (∼$2300, direct costs; ∼$400 indirect costs) than those who had surgery in the inpatient setting (IPH). More dramatic differences were observed, however, when comparing GEA with both OPH and IPH. We found that costs for women who had GEA are substantially less than the costs for women who had either OPH or IPH, with the difference (i.e., potential cost savings) ranging from approximately $7700 to approximately $10,000 for direct costs and approximately $4200 to approximately $4600 for indirect costs at the end of the year following OPH and IPH, respectively. Looking at the direct, gynecologic-related costs alone, GEA afforded cost savings for women relative to those who had hysterectomy, ranging from approximately $6600 to approximately $8100 at the end of the year following OPH and IPH, respectively.

Evaluation of costs of AUB treatment across different types of industries has never been performed before initiation of this study. The largest variances from the baseline (i.e., all industries combined) costs were observed in the industry classifications for ‘agriculture, forestry, fishing’, where 1-year costs following surgical AUB treatment were substantially less than the baseline (GEA: 28.4% less; OPH: 9.7% less), and for ‘oil and gas extraction, mining’ (IPH: 16.3% less). Similarly, the comparison of GEA versus hysterectomy showed that the largest cost differences were among the women (or their primary insurance policyholders) employed in ‘agriculture, forestry, fishing’ (i.e., cost savings of ~$9700 to ~$13,000 for GEA vs OPH and GEA vs IPH, respectively). Given the limitations of the data, there is difficulty in drawing any conclusions about these results, except to say that likely there are sociodemographic correlations and other confounding factors affecting the direction and magnitude of postsurgical AUB costs. The analyses and results we report here lay the rudimentary foundation for more sophisticated analyses that could take place in the future, particularly if specific employers can be niched into well-defined industry classifications.

Choice about type of surgical treatment of AUB has an important impact on a woman's return to work and subsequent work attendance. We observed that women undergoing GEA missed about 23 fewer days of work (i.e., about an entire month of standard 5-day work weeks) in the first year following surgery than those who opted for hysterectomy as their surgical AUB treatment. More than a half of these missed work days (∼13 days) were due to STD alone. Relative savings in indirect costs for GEA versus hysterectomy (amounting to more than $4000 in the year following surgical AUB treatment) certainly could be a meaningful lost value to employers across all industry types, but it could be most troublesome for small businesses where the loss of even one employee can make a significant impact on production and profit. Because absenteeism defined in the database used for this study includes family leave, vacation, holidays and jury duty in addition to sick leave, the hours of work absence specifically attributable to AUB certainly is a small subset of the total absence. However, this constraint consistently applies across all three surgical AUB treatments evaluated in the study, so the impact is negated when comparing results incrementally between treatments.

There is common acknowledgement that AUB is costly and has implications on women's functional employment and quality of life, but very few studies have quantitatively assessed the costs and impact of surgical AUB treatments on work productivity. The lead authors of this study previously published a similar study [11] using older data and drew similar conclusions about the relative value of GEA compared with hysterectomy in terms of direct and indirect costs. Most prior economic evaluations of AUB have focused on the work impact of AUB itself, rather than on the effects of its treatment [2,9,19]. In the most commonly cited example, Côté et al. [9] estimated that employed women with AUB would work 6.9% less, or 3.6 fewer weeks per year, with an average work loss cost attributable to AUB of $1692 (2000 USD) annually per woman. By contrast, Jensen et al. [19] estimated AUB attributable work-loss cost (including sick leave and disability costs) at only $74 per year. Frick et al. [8] estimated that women with AUB prior to surgery with hysterectomy or GEA miss about 4.5 h of paid work per month, resulting in an annual cost of $842 (2007 USD). Studies by Wasiak et al. [20,21] evaluated the work impact of estradiol-valerate/dienogest treatment on work productivity of women suffering from heavy menstrual bleeding across various countries. Results from the US analysis showed a 38% improvement in productivity from estradiol-valerate/dienogest treatment, with corresponding cost savings from improvement in work productivity estimated at $80 per month or $960 per year (2008 USD) [21]. By contrast, our study specifically examined all the women who had curative treatment for AUB and accounted for the follow-on direct and indirect costs of that treatment (whether ultimately successful or not) in the year following surgery.

A small (n = 67) cost-consequences study by Famuyide et al. [30] analyzed indirect costs of work loss due to AUB treatment among the women who were randomly allocated to receive medical therapy with oral contraceptive pills versus radiofrequency endometrial ablation (RFA), a specific type of GEA. Based on analyses of self-reported data, 1-year indirect costs (i.e., wages lost) specifically from reduced work days due to menstrual issues for women who had medical therapy or RFA were only $227 and $14, respectively. These estimates are magnitudes less than what we estimated in our study, owing largely to differences in the study methodologies, including the fact that we looked broadly at all types of paid absences and illness-related work loss that could be attributable to any condition, not restricted to AUB alone.

Finally, we mention our interest in the forthcoming results from the HEALTH (Hysterectomy or Endometrial AbLation Trial for Heavy menstrual bleeding) trial in the UK, a multicenter randomized controlled trial comparing laparoscopic supracervical hysterectomy with second-generation GEA in terms of clinical and cost–effectiveness [31]. One of the secondary outcome measures of the ongoing trial deals with work productivity (i.e., specifically, time lost from paid employment) following AUB surgical intervention.

The movement of employers toward recognizing the value of interventions to improve health and productivity, rather than just paying for the cost of healthcare, has become an important part of value-based decision making. With women comprising almost a half of the US workforce, and three-quarters of them of reproductive age (about 58 million women) [32], AUB may be an under-acknowledged health issue with important economic implications. Given that estimated annual direct costs of AUB in the USA range from $1 to $1.55 billion [2] (2005 USD) and indirect costs range from $12 to $36 billion [2] (2005 USD), safe, cost-effective treatments are appealing in today's cost-conscious healthcare environment. Results from this study could prove informative for policy decision making about costs and benefits of surgical treatment options for AUB, and, ultimately, about promoting economic empowerment of women in the workforce.

We believe results from this study will resonate especially with self-insured employers, as the percentage of workers enrolled in self-insured employer health plans has been increasing. In 2015, 39% of private-sector firms reported that they self-insured at least one of their health plans, and 60% of covered workers nationwide were enrolled in self-insured plans [33]. Applying these statistics to the approximately 58 million reproductive-age women in the workforce [32], it can be inferred that 35 million women receive healthcare coverage from self-insured employers, among whom about 20% or 7 million could have AUB (using the mid range of published AUB prevalence statistics) [2,3]. The population may be substantially larger if consideration is given to the additional, potentially large population of women receiving health insurance coverage from spouses and other primary policyholders working for self-insured employers. Even if only a small percentage of women with AUB would seek surgical treatment each year (and, unfortunately, statistics about this population are not readily available), the cumulative direct and indirect cost savings estimated in our study from choosing GEA over hysterectomy (up to $15,000 per patient) across this population would be quite sizeable.

Some strengths and limitations of this study bear mention. One of the major strengths of this study is that the sociodemographic profiles of the AUB treatment cohorts reflect real-world, observational data from employer-sponsored insurance claims. This is accomplished through the fact that the MarketScan databases underlying this study are naturalistic (unlike a clinical trial setting) and capture the full continuum of care: physician office visits; hospital stays; retail, mail order and specialty pharmacies; and carve-out care, such as mental health services [22,23]. Nonetheless, as with any data source, MarketScan data have limitations – some having to do with the nature of claims data and others with the nature of the MarketScan sample population. Key limitations of the data for this study include the fact that the MarketScan claims databases are based on a large norandom, convenience sample that may contain biases or fail to generalize to women utilizing surgical AUB treatments. As is true for any targeted selection of patient types from real-world data, there were observable differences between GEA and hysterectomy patients with regard to their demographic profiles and health histories. Our core analysis was purely descriptive of the naturalistic, real-world experience of self-insured employers with AUB patients in their health plans and may not fully account for the influence of sociodemographic and clinical factors that may affect treatment choices and outcomes. However, results from our exploratory multivariate analysis showed that such factors held little sway in the magnitude and direction of our core analysis cost estimates. The same conclusions hold about the lower healthcare costs associated with GEA versus OPH or IPH as surgical treatment options for women with AUB. Nonetheless, we do acknowledge that there may be unobservable differences between these women that were not reflected in the data available for our analysis, and that these differences may be of important concern for ascertaining healthcare utilization and costs.

For other limitations, we mention that procedure coding in claims data is limited in its ability to differentiate specific types/techniques of GEA or hysterectomy (although we are readily able to discern the location in which hysterectomy is performed – i.e., OPH and IPH). Further, the data in the MarketScan HPM Database come mostly from large employers; medium and small firms may be under-represented. We also point out that the indirect costs included in the analyses are not exhaustive. For example, absenteeism and STD claims do not include long-term disability, impaired on-the-job performance (‘presenteeism’) resulting in reduced work output, or job termination. Moreover, we cannot determine whether employers are absorbing the indirect costs through lower profits or employees are bearing the costs through lower wages and/or reductions in benefits. Finally, the timeframe of our analysis was limited to 1 year following intervention with GEA or hysterectomy. Although longer-term clinical sequelae and associated costs of these treatments were not included in the analysis, we believe that the 1-year timeframe adequately encompasses the period of greatest healthcare resource utilization after surgery and that the cost differential between GEA and hysterectomy would be sustained indefinitely. Findings from the cost–effectiveness studies of AUB treatment by Spencer et al. [34] and Roberts et al. [35] substantiate our assertion looking at economic outcomes over 5- and 10-year time horizons, respectively.

Conclusion

While health insurance traditionally covers direct healthcare costs related to the treatment of illness and disease, the indirect costs of poor health are also of increasing concern to employers. A growing number of self-insured employers are taking a more balanced view of providing employee health-related benefits, with a belief that spending on employee health and wellness is an investment in human capital. More and better information on the value of healthcare services/treatment is being sought by employers investing in the health and productivity of female employees and for those looking to optimize their medical plans through value-based insurance designs [36,37]. With women comprising such a high percentage of the workforce and AUB being such a highly prevalent and expensive condition among reproductive age women, employers, particularly those self-insured, will be keenly interested in these analyses presented here which show lower healthcare costs associated with GEA versus OPH or IPH as a surgical treatment option for women with AUB.

•

Millions of women in the workforce suffer from abnormal uterine bleeding (AUB; 10–30% of women of reproductive age).

•

AUB can impact a woman's ability to perform paid work, with potential financial impact on both herself and her employer.

•

AUB is an expensive condition to endure and to treat, and choice of treatments can profoundly affect costs.

•

The objective of this study was to analyze costs associated with surgical treatment options for AUB from the perspective of self-insured employers.

•

Employer-sponsored insurance claims data were analyzed to estimate costs due to absence and short-term disability 1 year following global endometrial ablation (GEA), outpatient hysterectomy and inpatient hysterectomy.

•

Results from this study show 1-year combined direct and indirect costs for women undergoing surgical treatment for AUB ranged from $21,000 (GEA) to $33,000 (outpatient hysterectomy) and $36,000 (inpatient hysterectomy).

•

From an employer's perspective, women with AUB who had GEA incurred substantially lower ($7700–$10,000) direct costs and lower ($4200–$4,600) indirect costs compared with those who had hysterectomy.

•

Results from this study emphasize the importance for healthcare providers to be aware that choice about type of surgical treatment of AUB impacts a woman's work attendance and the cost burden to her employer.

Author contributions

This study was conceived and designed by JD Miller and SK Pohlman. Data collection and analyses were performed by JD Miller and MM Bonafede. All authors contributed to the data analyses interpretation, drafting, revision and approval of the submitted manuscript.

Acknowledgments

The authors thank Jake Flaitz, Director of Benefits at Paychex, for his assistance in reviewing draft versions of this manuscript. The authors also express appreciation to Qian Cai for assistance with conducting data analyses.

Financial & competing interests disclosure

This study was sponsored by Hologic, Inc., Marlborough, MA, USA. JD Miller and MM Bonafede are employees of IBM Watson Health, which received funding from Hologic, Inc. Also, SK Pohlman and KA Troeger are employees of Hologic, Inc., which provided funding to conduct the study. A Cholkeri-Singh is a paid consultant to Hologic, Inc., but she received no financial compensation for her contribution to this particular study. The authors have no other relevant affiliations or financial involvement with any organization or entity with a financial interest in or financial conflict with the subject matter or materials discussed in the manuscript apart from those disclosed.

No writing assistance was utilized in the production of this manuscript.

Ethical conduct of research

The authors state that all database records analyzed for this study were de-identified and fully compliant with the US patient confidentiality requirements, including the Health Insurance Portability and Accountability Act of 1996. Institutional review board approval to conduct this study was not required because the study uses only de-identified patient records and does not involve the collection, use or transmittal of individually identifiable data.

Open access

This work is licensed under the Attribution-NonCommercial-NoDerivatives 4.0 Unported License. To view a copy of this license, visit http://creativecommons.org/licenses/by-nc-nd/4.0/

References

Papers of special note have been highlighted as: • of interest; •• of considerable interest

1.

American College of Obstetricians and Gynecologists (ACOG). Frequently asked questions, gynecologic problems: abnormal uterine bleeding. patient education pamphlet, FAQ095 (2017). www.acog.org/Patients/FAQs/Abnormal-Uterine-Bleeding

2.

Liu Z, Doan QV, Blumenthal P, Dubois RW. A systematic review evaluating health-related quality of life, work impairment, and health-care costs and utilization in abnormal uterine bleeding. Value Health 10(3), 183–194 (2007).

•• Provides widely cited estimates of the annual direct costs of abnormal uterine bleeding (AUB) in the USA, ranging from $1 to $1.55 billion (2005 USD) and indirect costs ranging from $12 to $36 billion (2005 USD).

3.

Centers for Disease Control and Prevention (CDC). Bleeding disorders in women: heavy menstrual bleeding (2017). www.cdc.gov/ncbddd/blooddisorders/women/menorrhagia.html

4.

Whitaker L, Critchley HO. Abnormal uterine bleeding. Best Pract. Res. Clin. Obstet. Gynaecol. 34, 54–65 (2016).

5.

Matteson KA, Raker CA, Clark MA, Frick KD. Abnormal uterine bleeding, health status, and usual source of medical care: analyses using the Medical Expenditures Panel Survey. J. Womens Health (Larchmt.) 22(11), 959–965 (2013).

6.

Fraser IS, Langham S, Uhl-Hochgraeber K. The health-related quality of life and economic burden of abnormal uterine bleeding: a critical review. Expert Rev. Obstet. Gynecol. 4, 179–189 (2009).

7.

National Institute for Health and Care Excellence (NICE). Heavy menstrual bleeding: assessment and management. NICE Guideline NG88 (2018). www.nice.org.uk/guidance/ng88/resources/heavy-menstrual-bleeding-assessment-and-management-pdf-1837701412549

8.

Frick KD, Clark MA, Steinwachs DM et al. Financial and quality-of-life burden of dysfunctional uterine bleeding among women agreeing to obtain surgical treatment. Womens Health Issues 19(1), 70–78 (2009).

• Estimates that women with AUB prior to surgery with hysterectomy or global endometrial ablation (GEA) miss about 4.5 h of paid work per month, resulting in an annual cost of $842 (2007 USD).

9.

Côté I, Jacobs P, Cumming D. Work loss associated with increased menstrual loss in the United States. Obstet. Gynecol. 100(4), 683–687 (2002).

• Estimated that employed women with AUB would work 6.9% less, or 3.6 fewer weeks per year, with an average work loss cost attributable to AUB of $1692 (2000 USD) annually per woman.

10.

Miller JD, Bonafede MM, Cai Q, Pohlman SK, Troeger KA, Cholkeri-Singh A. Economic evaluation of global endometrial ablation versus inpatient and outpatient hysterectomy for treatment of abnormal uterine bleeding: US commercial and Medicaid payer perspectives. Popul. Health. Manag. 21(S1), S1–S12 (2018).

•• Robust economic modeling analyses with results suggesting strong financial favorability for GEA versus outpatient hysterectomy or inpatient hysterectomy from both the commercial and Medicaid perspectives.

11.

Bonafede MM, Miller JD, Lukes A, Meyer NM, Lenhart GM. Comparison of direct and indirect costs of abnormal uterine bleeding treatment with global endometrial ablation and hysterectomy. J. Comp. Eff. Res. 4(2), 115–122 (2015).

•• Similar study using older data but drawing similar conclusions about the relative value of GEA compared with hysterectomy in terms of direct and indirect costs.

12.

American College of Obstetricians and Gynecologists. ACOG committee opinion no. 557: management of acute abnormal uterine bleeding in nonpregnant reproductive-aged women. Obstet. Gynecol. 121(4), 891–896 (2013).

13.

Oehler MK, Rees MC. Menorrhagia: an update. Acta Obstet. Gynecol. Scand. 82, 405–422 (2003).

14.

Apgar BS, Kaufman AH, George-Nwogu U, Kittendorf A. Treatment of menorrhagia. Am. Fam. Physician 75(12), 1813–1819 (2007).

15.

Stovall DW. Alternatives to hysterectomy: focus on global endometrial ablation, uterine fibroid embolization, and magnetic resonance-guided focused ultrasound. Menopause 18(4), 437–444 (2011).

16.

Munro MG. Endometrial ablation. Best Pract. Res. Clin. Obstet. Gynaecol. 46, 120–139 (2018).

17.

Billow MR, El-Nashar SA. Management of abnormal uterine bleeding with emphasis on alternatives to hysterectomy. Obstet. Gynecol. Clin. N. Am. 43(3), 415–430 (2016).

18.

Laberge P, Leyland N, Murji A et al. Endometrial ablation in the management of abnormal uterine bleeding. J. Obstet. Gynaecol. Can. 37(4), 362–379 (2015).

19.

Jensen JT, Lefebvre P, Laliberté F et al. Cost burden and treatment patterns associated with management of heavy menstrual bleeding. J. Womens Health (Larchmt.) 21, 539–547 (2012).

• Estimated AUB-attributable work-loss cost (including sick leave and disability costs) at only $74 per year.

20.

Wasiak R, Filonenko A, Vanness DJ et al. Impact of estradiol-valerate/dienogest on work productivity and activities of daily living in European and Australian women with heavy menstrual bleeding. Int. J. Womens Health 4, 271–278 (2012).

21.

Wasiak R, Filonenko A, Vanness DJ et al. Impact of estradiol valerate/dienogest on work productivity and activities of daily living in women with heavy menstrual bleeding. J. Womens Health (Larchmt.) 22(4), 378–384 (2013).

22.

IBM Watson Health. IBM MarketScan Research Databases (2019). www.ibm.com/us-en/marketplace/marketscan-research-databases and https://www.ibm.com/downloads/cas/JMPKEDA5

23.

IBM Watson Health. White paper: IBM MarketScan Research Databases for health services researchers (2019). www.ibm.com/downloads/cas/6KNYVVQ2

24.

Berger ML, Murray JF, Xu J, Pauly M. Alternative valuations of work loss and productivity. J. Occup. Environ. Med. 43(1), 18–24 (2001).

25.

Pauly MV, Nicholson S, Xu J et al. A general model of the impact of absenteeism on employers and employees. Health Econ. 11(3), 221–231 (2002).

26.

Mattke S, Balakrishnan A, Bergamo G, Newberry SJ. A review of methods to measure health-related productivity loss. Am. J. Manag. Care 13(4), 211–217 (2007).

27.

United States Department of Labor, Bureau of Labor Statistics. News Release (19 July 2017), ‘Usual weekly earnings of wage and salary workers, second quarter 2017’ (2017). www.bls.gov/news.release/archives/wkyeng_07192017.pdf

28.

United States Department of Labor, Bureau of Labor Statistics. Databases, Tables & Calculators by Subject: Employment, Hours, and Earnings from the Current Employment Statistics Survey (National), Series CS0500000002, “Average weekly hours of all employees, total private, seasonally adjusted” (December 2017 data extracted on 13 March 2018) (2018). https://data.bls.gov/timeseries/CES0500000002

29.

United States Department of Labor, Bureau of Labor Statistics. Employee benefits survey, ‘Table 26. Short-term disability plans: fixed percent of annual earnings, private industry workers’ (March 2017) (2017). www.bls.gov/ncs/ebs/benefits/2017/ownership/private/table26a.pdf

30.

Famuyide AO, Laughlin-Tommaso SK, Shazly SA et al. Medical therapy versus radiofrequency endometrial ablation in the initial treatment of heavy menstrual bleeding (iTOM Trial): a clinical and economic analysis. PLoS ONE 12(11), e0188176 (2017).

• Estimated 1-year indirect costs (i.e., wages lost) specifically from reduced work days due to menstrual issues for women who had medical therapy or radiofrequency endometrial ablation were only $227 and $14, respectively.

31.

Cooper K, McCormack K, Breeman S et al. HEALTH: laparoscopic supracervical hysterectomy versus second-generation endometrial ablation for the treatment of heavy menstrual bleeding: study protocol for a randomised controlled trial. Trials 19(1), 63 (2018).

32.

United States Department of Labor, Bureau of Labor Statistics. Women in the labor force: a databook. Report 1071 (November 2017) (2017). www.bls.gov/opub/reports/womens-databook/2017/home.htm

33.

Fronstin P. Self-insured health plans: recent trends by firm size, 1996–2015. Employee Benefit Research Institute Notes 37(7), 2–6 (2016). www.ebri.org/pdf/notespdf/EBRI_Notes_07-no7-July16.Self-Ins.pdf

34.

Spencer JC, Louie M, Moulder JK et al. Cost-effectiveness of treatments for heavy menstrual bleeding. Am. J. Obstet. Gynecol. 217(5), 574.e1–574.e9 (2017).

35.

Roberts TE, Tsourapas A, Middleton LJ et al. Hysterectomy, endometrial ablation, and levonorgestrel releasing intrauterine system (Mirena) for treatment of heavy menstrual bleeding: cost effectiveness analysis. BMJ 342, d2202 (2011).

36.

Gibson TB, Maclean RJ, Chernew ME, Fendrick AM, Baigel C. Value-based insurance design: benefits beyond cost and utilization. Am. J. Manag. Care 21(1), 32–35 (2015).

37.

Robinson JC. Applying value-based insurance design to high-cost health services. Health Aff. (Millwood) 29(11), 2009–2016 (2010).

Information & Authors

Information

Published In

Pages: 67 - 77

PubMed: 31773992

Copyright

© 2019 Miller et al. This work is licensed under the Attribution-NonCommercial-NoDerivatives 4.0 Unported License

History

Received: 18 July 2019

Accepted: 28 October 2019

Published online: 27 November 2019

Keywords:

Topics

Authors

Metrics & Citations

Metrics

Article Usage

Article usage data only available from February 2023. Historical article usage data, showing the number of article downloads, is available upon request.

Citations

How to Cite

Employer-perspective cost comparison of surgical treatments for abnormal uterine bleeding. (2019) Journal of Comparative Effectiveness Research. DOI: 10.2217/cer-2019-0102

Export citation

Select the citation format you wish to export for this article or chapter.